Polymarket arbitrage exists because two different pricing systems are assessing the same outcome at the same time and arriving at different numbers. Polymarket's peer-to-peer order book, driven by a global crowd of capital-backed traders, prices events differently from a sportsbook that embeds a profit margin into every line and adjusts based on its own risk position. When those two pricing systems disagree enough to cover the transaction costs on both sides, an arbitrage opportunity exists

The gap is real, documented, and exploitable. One head-to-head test found DraftKings posting -132 on a moneyline where the Polymarket equivalent contract was priced at 58.5 cents, a 1.1 cent difference after adjusting for sportsbook vig on the same game. During the 2026 World Cup, documented gaps of 5 to 8 percentage points appeared between Polymarket and Kalshi on the same team's winner odds. These are not edge cases. They are recurring features of how two structurally different pricing systems respond to the same information at different speeds.

This guide explains why those gaps exist, how to read the two odds formats against each other, and a practical 10-minute workflow for identifying and sizing the opportunities before they close. For the foundational mechanics of how Polymarket prices work as probability estimates, Polymarket explained: how prediction markets work covers the complete framework before you start comparing them to sportsbook lines.

Why Price Discrepancies Between Polymarket and Sportsbooks Exist

Understanding why the gaps appear is the prerequisite for finding them consistently. There are four structural reasons why Polymarket and sportsbooks price the same outcome differently, and each one creates a different type of arbitrage opportunity.

The big difference

Sportsbooks embed a profit margin into every line. A standard -110/-110 NFL spread market at DraftKings implies 52.4% probability on each side of a 50-50 event. The true probability is 50%. The 2.4-point difference on each side is the vig made visible. Polymarket charges no vig on most major sports markets, meaning its prices reflect the market's actual probability estimate without a house margin distorting the output.

This structural difference means that a sportsbook line and a Polymarket price on the same outcome will almost always show a gap when you compare them. The question is whether that gap is larger than the vig adjustment alone, because a gap equal to the vig is not arbitrage. It is the expected difference between a vig-embedded line and a vig-free prediction market price.

A genuine polymarket arbitrage opportunity exists when the gap exceeds the vig adjustment by enough to cover your transaction costs on both sides. That threshold is typically 3 to 5 percentage points above the vig adjustment on liquid markets.

The repricing speed difference

Polymarket replicates in real time as traders act on new information. A sportsbook has a line adjustment process that involves human review or algorithmic oversight before a new price is offered. When significant information breaks, whether an injury report, a weather update, or a regulatory announcement, Polymarket typically reflects that information within minutes. Sportsbooks typically take 15 to 30 minutes to fully adjust.

That repricing speed gap creates a narrow but real arbitrage window after major information events. A trader who can position on both sides of the gap within the first 10 to 15 minutes after information breaks captures the difference between Polymarket's fast reprice and the sportsbook's slower adjustment. The window closes as the sportsbook catches up.

The audience composition difference

Polymarket's global user base prices European and South American sports with more accuracy than US-centric sportsbooks. A Kalshi or DraftKings line on a Champions League match is priced primarily by an American audience that may underweight specific team quality factors that Polymarket's European traders have correctly assessed.

This audience composition gap is most visible in international soccer, where Polymarket's global crowd consistently produces tighter lines on European team quality than US-facing platforms. The gap is smaller on NFL and NBA markets where both audiences have comparable information and comparable depth of knowledge.

Read More: Polymarket Supported and Restricted Countries

The information processing difference

Sportsbook lines are set by oddsmakers who price based on public information and their own risk management. Polymarket prices are set by thousands of traders, some of whom have proprietary research, better models, or faster access to primary sources. When the Polymarket crowd has priced in information that the sportsbook has not yet incorporated, a gap appears that reflects genuine information asymmetry rather than structural vig differences.

Explore Live Prediction Markets

How to Read and Compare Odds Formats

The first mechanical skill required for prediction market vs sportsbook odds arbitrage is converting between Polymarket's probability format and sportsbook American or decimal odds. Without this conversion, you cannot identify whether a gap is real or illusory.

Converting Polymarket prices to American odds

Polymarket prices are expressed as probability in dollar terms. A $0.62 contract means 62% implied probability.

For favorites above $0.50: American odds = minus (price divided by (1 minus price)) multiplied by 100. A $0.62 contract converts to approximately -163.

For underdogs below $0.50: American odds = ((1 minus price) divided by price) multiplied by 100. A $0.38 contract converts to approximately +163.

Converting sportsbook American odds to implied probability

For negative American odds (favorites): implied probability = (absolute value of odds) divided by (absolute value of odds plus 100). A -163 line implies 62% probability.

For positive American odds (underdogs): implied probability = 100 divided by (odds plus 100). A +163 line implies 38% probability.

The vig adjustment

Sportsbook implied probabilities always sum to more than 100% because the vig is embedded in both sides. To get the vig-adjusted true probability from a sportsbook line, divide each side's implied probability by the total implied probability of both sides combined.

Example: a -110/-110 market gives 52.4% on each side, summing to 104.8%. Vig-adjusted probability is 52.4% divided by 104.8%, which equals 50%. That is the sportsbook's actual view of the true probability, stripped of the margin.

When you compare the vig-adjusted sportsbook probability to the Polymarket price on the same outcome, any remaining gap after the vig adjustment is either genuine information asymmetry or structural differences in how the two audiences assess the event. That gap is what you are looking for.

The comparison table you need

For the application of this odds comparison framework to NFL player prop markets specifically, NFL player props on Polymarket: advanced stats covers how to use the probability comparison to identify statistical edges on player-level contracts. For the platform comparison of when Kalshi or Polymarket offers better pricing on the same sports outcome, Kalshi vs Polymarket: which is better for sports covers the head-to-head.

The 10-Minute Arbitrage Workflow

The workflow below identifies genuine arbitrage opportunities in under 10 minutes using two data sources:

Step 1: Identify the target market category (Minutes 1 to 2)

Not all market categories produce comparable arbitrage opportunities. Start with the categories where structural gaps are most consistently documented.

Major sports futures including NFL Champion, NBA Champion, and World Cup winner markets consistently show the largest vig-adjusted gaps because the long duration of these markets creates more opportunity for the two pricing systems to diverge. A six-month futures market on a team's championship probability has more time to develop genuine information asymmetry than a same-day game market.

International soccer is the second-best category because of the audience composition difference between Polymarket's global crowd and US-centric sportsbooks. Champions League and World Cup markets on European teams regularly show 3 to 6 percentage point vig-adjusted gaps.

Same-day game markets on major US sports are the most efficient category because both pricing systems receive the same information at roughly the same time and the arbitrage window after information events is shortest.

Step 2: Pull the Polymarket price and convert it (Minutes 2 to 4)

Open the relevant market on polymarket.com and note the current price for the outcome you are evaluating. Convert it to American odds using the formula above. This is your baseline probability estimate from the prediction market.

Also check the order book depth before proceeding. If there are fewer than 500 shares available at the current price, the market is too thin for any meaningful position without significant slippage. Move to the next market.

Read more: Best Polymarket Markets to Trade in 2026

Step 3: Find the vig-adjusted sportsbook probability (Minutes 4 to 6)

Open oddschecker.com and find the same outcome across multiple sportsbooks. Record the American odds from at least three books: DraftKings, FanDuel, and one additional sharp book like Pinnacle if the market is available.

Calculate the vig-adjusted implied probability for each book and take the average. That average is the sportsbook consensus view of true probability, stripped of the house margin.

Compare the vig-adjusted sportsbook consensus to the Polymarket price. The gap between them is your raw arbitrage signal.

Step 4: Assess the gap against your minimum threshold (Minutes 6 to 8)

A raw gap of any size is not sufficient. You need the gap to clear three thresholds before entering a position.

The transaction cost threshold: the gap must exceed the round-trip cost of entering and exiting positions on both platforms. On Polymarket, this is the spread cost on entry and exit. On the sportsbook side, this is the vig embedded in the line. A conservative minimum gap after both adjustments is 3 percentage points.

The liquidity threshold: the gap must be available at sufficient size on both sides to make the position worth executing. A 5-percentage-point gap on a Polymarket market with $8,000 in volume allows meaningful sizing. The same gap on a $2,000 volume market does not.

The timing threshold: the gap must have been stable for at least 5 to 10 minutes without either side repricing toward the other. A gap that appeared 30 seconds ago when a news story broke is likely to close before you can execute both sides. A gap that has been stable for 15 minutes is more likely to persist long enough for full execution.

Step 5: Execute and set exit parameters (Minutes 8 to 10)

If all three thresholds are cleared, execute the position. Buy the underpriced side on Polymarket and either back the opposite outcome on the sportsbook or sell the overpriced side if a selling mechanism is available.

Set your exit parameters before entering. On the Polymarket side, set a limit sell order at the price that captures your target profit margin if the market moves to fair value. On the sportsbook side, your position is locked until resolution unless a cash-out option is available at an acceptable price.

For Kalshi-specific arbitrage strategies that use the same workflow between Kalshi and Polymarket rather than sportsbooks, Kalshi prediction market: 7 strategies that work in 2026 covers the cross-platform approach in detail.

Risks and Limits That Most Arbitrage Guides Skip

The execution risk

Polymarket arbitrage requires executing both sides of the trade within a narrow time window. If the Polymarket side fills at your target price but the sportsbook line moves before you complete the sportsbook side, you are left with a one-sided position rather than a hedged arbitrage. That one-sided position is a directional bet with full outcome risk, not an arbitrage.

The risk of this happening increases in fast-moving markets immediately after news breaks. The same information that created the gap can close it before you complete both sides of the trade.

The liquidity risk on Polymarket

Even on markets with substantial total volume, the order book depth at any specific price may be insufficient for your target position size. Entering a large position on a thin order book moves the price against you and reduces the effective gap you are trading. Calculate your effective entry price across the full position size, not just at the top of the book, before committing.

The withdrawal friction risk

Polymarket arbitrage profits require being able to move money between platforms efficiently. Polymarket's global platform settles in USDC on Polygon, which then needs to be converted and moved to a bank account. Sportsbooks settle in fiat with their own processing timelines. The friction of moving capital between platforms reduces the effective return on any arbitrage strategy that depends on rapid capital recycling.

This friction is less severe on the Polymarket US platform that accepts fiat deposits, but the market depth on the US platform is shallower than on the global platform, which reduces the available arbitrage opportunities.

The account limitation risk on sportsbooks

Sportsbooks that identify accounts as sharp bettors or arbitrage traders routinely limit or ban those accounts. If your sportsbook activity pattern suggests you are systematically fading the house margin, your account will eventually be restricted. This risk does not apply on the Polymarket side, which does not limit profitable traders, but it applies fully on the sportsbook side of any arbitrage strategy.

For the complete framework on managing capital across multiple platforms including risk limits and position sizing for arbitrage strategies, the prediction market bankroll management guide covers the methodology.

Frequently Asked Questions

What is Polymarket arbitrage and how does it work?

Polymarket arbitrage involves identifying situations where the same outcome is priced differently on Polymarket and on a sportsbook, then taking opposing positions on both platforms to profit from the price difference regardless of which side wins. The gap exists because Polymarket's peer-to-peer order book and a sportsbook's vig-embedded line are produced by different pricing mechanisms with different structural costs. When the gap between the two prices exceeds the transaction costs on both sides, a genuine arbitrage opportunity exists.

How do you find price discrepancies between Polymarket and sportsbooks?

Convert the Polymarket price to implied probability. Then calculate the vig-adjusted implied probability from the sportsbook line by dividing each side's implied probability by the total implied probability summed across both sides. Compare the two numbers. Any gap above 3 percentage points that has been stable for at least 10 minutes and is available at sufficient order book depth on both sides is worth evaluating as a potential arbitrage opportunity. On polymarket arbitrage reddit, the prediction markets subreddit carries active community discussion of specific gap opportunities as they appear across different sports categories.

Is arbitrage trading on Polymarket legal?

Trading on Polymarket is legal for US residents in eligible states following the December 2025 US relaunch under CFTC oversight. Nine states have active restrictions. Arbitrage strategies that involve simultaneously holding positions on Polymarket and a licensed sportsbook are legal trading activities. The only legal risk is on the sportsbook side, where systematic arbitrage activity may cause the sportsbook to limit or close your account, which is a commercial action rather than a legal one.

How much can you realistically make from Polymarket arbitrage?

The realistic return from systematic Polymarket arbitrage depends on your capital base, the frequency of genuine opportunities, and the liquidity available at each opportunity. Academic research on Polymarket found that arbitrageurs extracted over $40 million in risk-free profits between April 2024 and April 2025, with the top three wallets alone earning $4.2 million. However, those figures reflect sophisticated multi-market systematic strategies rather than manual sportsbook-versus-Polymarket arbitrage. For a retail trader executing the 10-minute workflow manually, realistic returns are lower and depend heavily on the frequency of opportunities that clear all three thresholds in the specific sports categories you are monitoring.

The Bottom Line

Polymarket arbitrage between prediction markets and sportsbooks is real, recurring, and exploitable with a consistent workflow. The gaps exist because two structurally different pricing systems respond to the same information at different speeds, with different cost structures, and from audiences with different information advantages on specific market categories.

The 10-minute workflow gives you a systematic process for identifying which gaps are genuine after adjusting for vig, checking liquidity, and confirming stability before committing capital to both sides of the trade. The risks are execution timing, order book depth, withdrawal friction, and sportsbook account limitation, all of which are manageable with the right position sizing and platform awareness.

The categories with the most consistent opportunities are major sports futures where long duration creates more time for the two systems to diverge, and international soccer where Polymarket's global audience systematically outprices US-centric sportsbooks on European team quality.

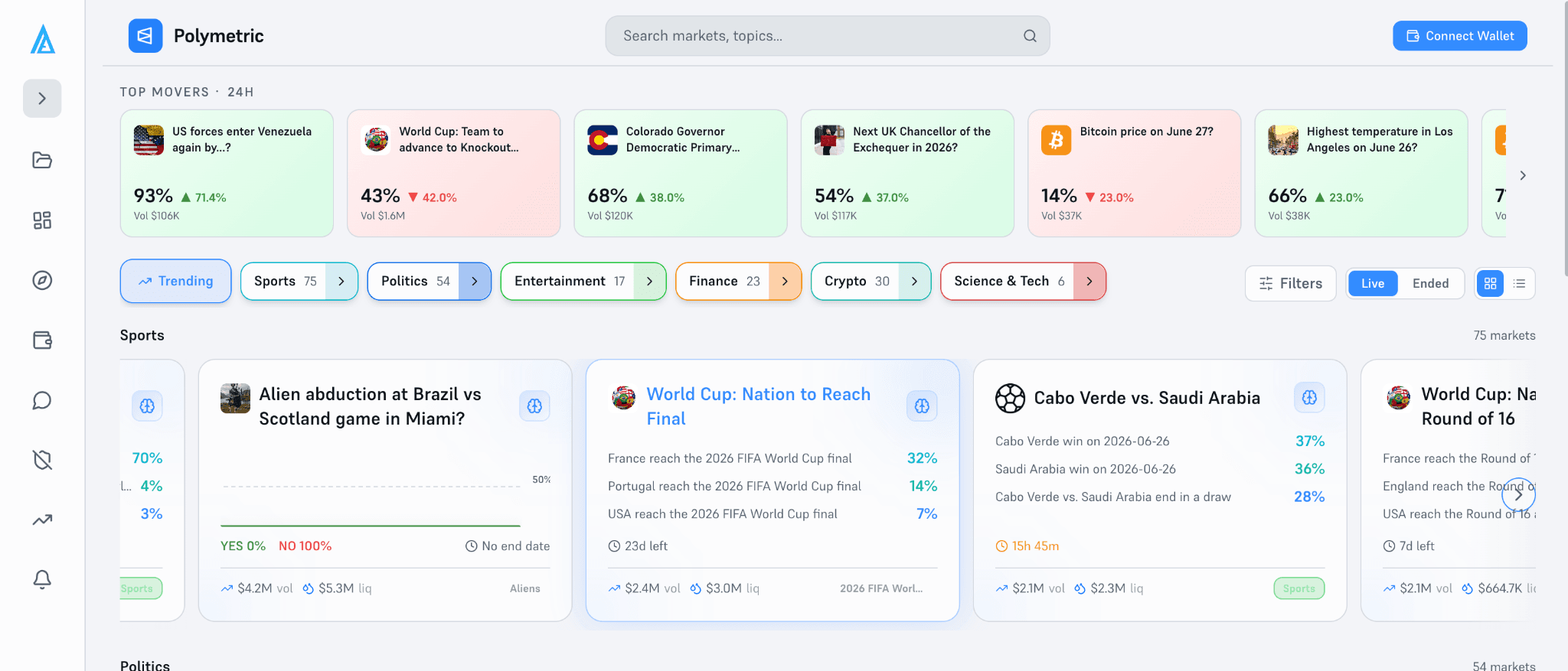

Track how Polymarket sports prices move in real time across every active contract with Polymetric by Laika AI. Live market intelligence for arbitrage traders who need to see price gaps the moment they open.