Most traders lose money in prediction markets not because they pick the wrong outcomes, but because they risk too much on each trade. Proper bankroll management is the difference between surviving long enough for your edge to compound and blowing up your account in a single bad week.

This guide provides the exact framework, with real position sizing examples, Kelly criterion calculations, and the drawdown rules that serious traders actually use.

Why Bankroll Management Works Differently in Prediction Markets

Every prediction market contract resolves at exactly $1.00 or $0.00. There is no middle ground, no stop-loss you can set at $0.85, no partial exit at a better price if the market moves against you. This binary structure makes position sizing fundamentally different from equities or crypto trading, where you can cut losses at 10% or 15%.

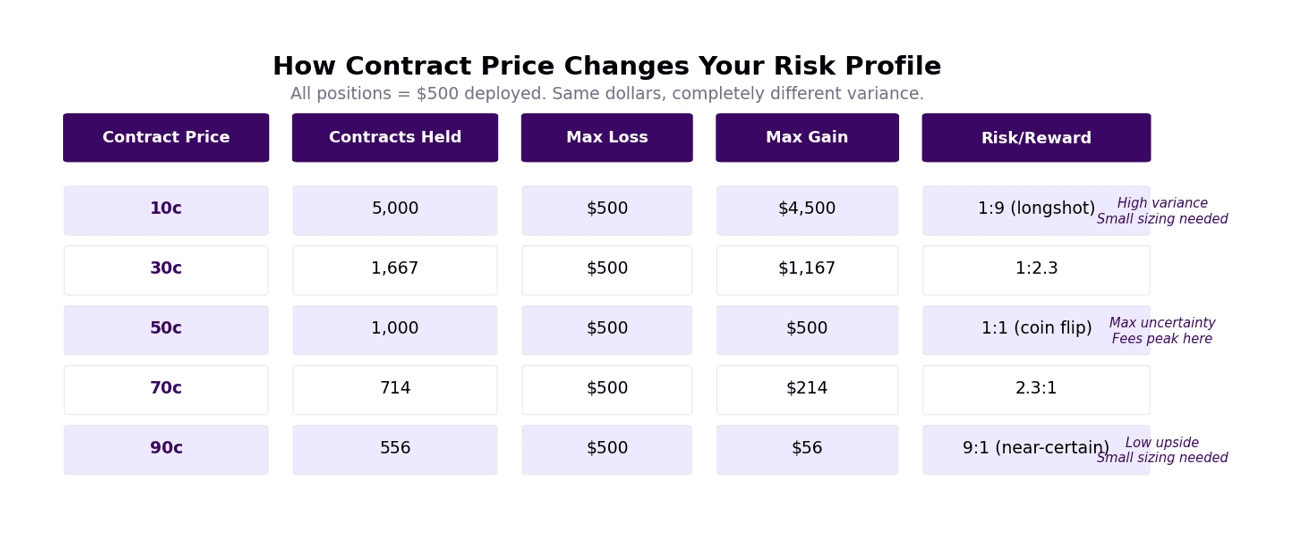

The contract price itself changes your risk profile even when the dollar position stays constant. A $500 bet at 10c means you're holding 5,000 contracts with a maximum loss of $500 but maximum gain of $4,500. That same $500 at 90c means only 556 contracts with a maximum gain of just $56. Both are $500 positions, but they carry completely different variance profiles that demand different sizing approaches.

Step One: Define Your Trading Bankroll Before You Place Any Trade

How much to risk in prediction markets starts with separating trading capital from savings. Pick a fixed number you are comfortable losing entirely. Your rent money, emergency fund, and long-term investments are not your prediction market bankroll. All position sizing is a percentage of this dedicated number.

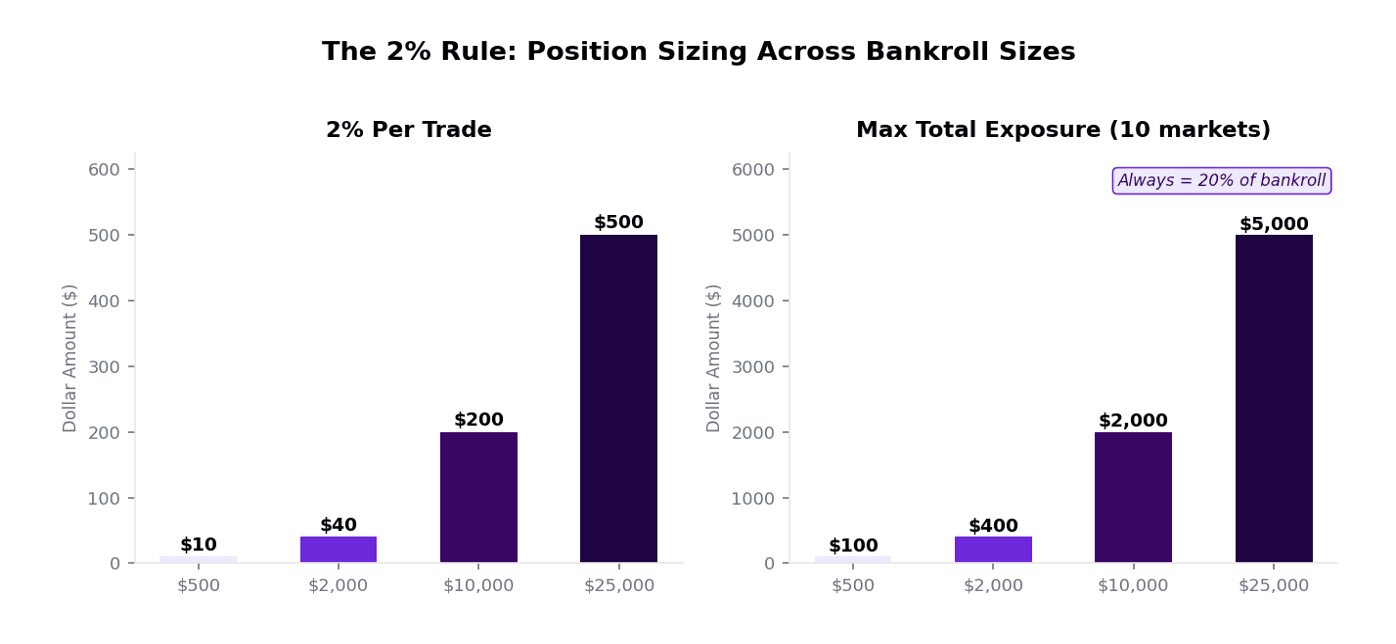

For consistency throughout this guide, a $2,000 trading bankroll is used as the anchor example. Every calculation scales from this number. If your actual bankroll is $500, divide by 4. If it is $10,000, multiply by 5.

Critical Rule: Your bankroll is the number you start with, not your current balance. If you start with $2,000 and grow to $2,400, your position sizing still uses $2,000 as the base until you explicitly decide to rebase your bankroll. This is recommended quarterly, not daily.

Why this matters: Using current balance creates a psychological trap where winning streaks encourage oversizing and losing streaks force undersizing, exactly when you should maintain discipline.

The Fixed Percentage Method: The Right Starting Point for Most Traders

The simplest and most sustainable approach is risking a fixed percentage of your bankroll per market, typically 1 to 5%, with 2% as the default.

Why 2% is the standard

Allows 50 trades before complete bankroll depletion (theoretically)

Protects against correlation risk when holding multiple positions

Psychologically manageable during losing streaks

Proven across poker, sports betting, and prediction markets

When to increase to 5%

You have 100 or more resolved trades documenting genuine edge

Win rate consistently exceeds 60% with positive expected value

You understand the increased variance and can handle 30%+ drawdowns

Why 20% total exposure is the ceiling: Once you exceed 20% of bankroll deployed across active positions, correlation risk becomes unmanageable. If multiple markets depend on the same underlying event, they can all resolve against you simultaneously, creating drawdowns exceeding 50%.

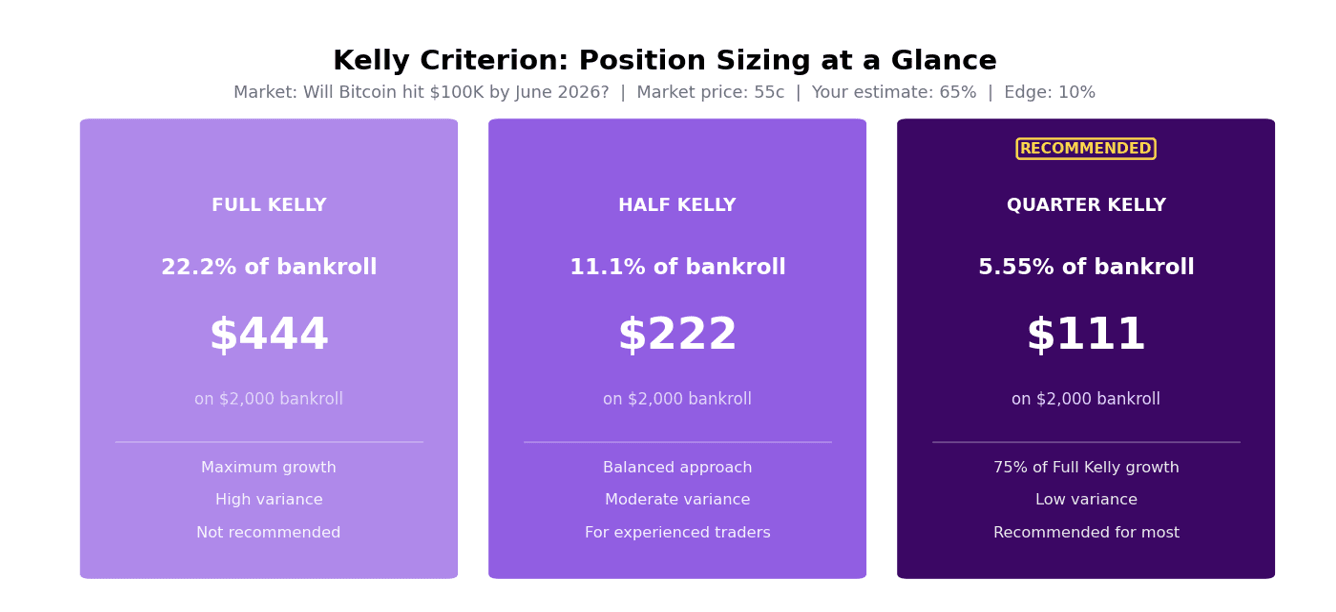

Kelly Criterion for Prediction Markets: Sizing by Edge, Not Instinct

The Kelly criterion is a mathematical formula that calculates optimal position size based on your estimated edge. Unlike fixed percentage methods, Kelly adjusts position size dynamically: bigger bets when you have a strong edge, smaller bets when edge is marginal.

The Formula

Kelly % = (Edge / Odds) x 100 Edge = Your estimated probability minus the market price Odds = Payout if you win (for YES contracts: 1 minus market price) |

Worked Example: $2,000 Bankroll

Market: Will Bitcoin hit $100K by June 2026? Market price: 55c. Your estimated true probability: 65%. Your edge: 10 percentage points.

What you should actually do: Use Quarter Kelly as your ceiling. Full Kelly maximizes long-run growth mathematically but produces drawdowns of 30 to 50% that are psychologically impossible for most traders to hold through. Quarter Kelly delivers roughly 75% of Full Kelly's growth with far more manageable variance.

When to reduce further below Quarter Kelly

Market liquidity is thin (slippage risk increases)

You are already holding correlated positions

Recent drawdown exceeds 15%

Contract price is below 20c or above 80c (extreme variance zones)

How Contract Price Changes the Risk Profile of Every Position

This is the critical insight most prediction market traders miss: a $500 position at 10c is structurally different from $500 at 90c, even though the nominal dollar risk is identical.

Key Takeaways

Longshot contracts (10c to 20c): need smaller dollar sizing because you hold more contracts with higher variance. A $500 position at 10c means 5,000 contracts. The high contract count amplifies both volatility and emotional weight.

Near-certain contracts (80c to 90c): need smaller sizing because the upside does not justify concentration risk. A $500 position at 90c risks $500 to win just $56. You need a 9:1 win rate just to break even, and one upset wipes out nine wins.

The 50c zone: is where sizing discipline matters most. Risk and reward are equal at 1:1 and fees peak simultaneously on most platforms. This is where poor position sizing destroys accounts fastest.

How Many Markets Should You Have Open at Once?

Correlation is the hidden bankroll killer. Two political markets that both depend on the same election outcome are not two independent bets. They are one bet split across two venues. If a candidate loses a state, all your related positions resolve to $0 simultaneously.

How to spot correlated markets

Same underlying event (multiple markets on the same election)

Same resolution date (all resolving on the same day)

Same directional exposure (all benefit from one outcome)

Dependent outcomes (if A happens, B becomes more likely)

The correlation rule: Never hold more than 20% of bankroll in correlated outcomes regardless of how many separate markets they sit across.

Here is the properly formatted table:

| Bankroll | Max Concurrent Markets | Max in Correlated Group |

|---|---|---|

| $500 | 5 | 2 |

| $2,000 | 10 | 3 |

| $10,000 | 15 | 4 |

| $25,000 | 20 | 5 |

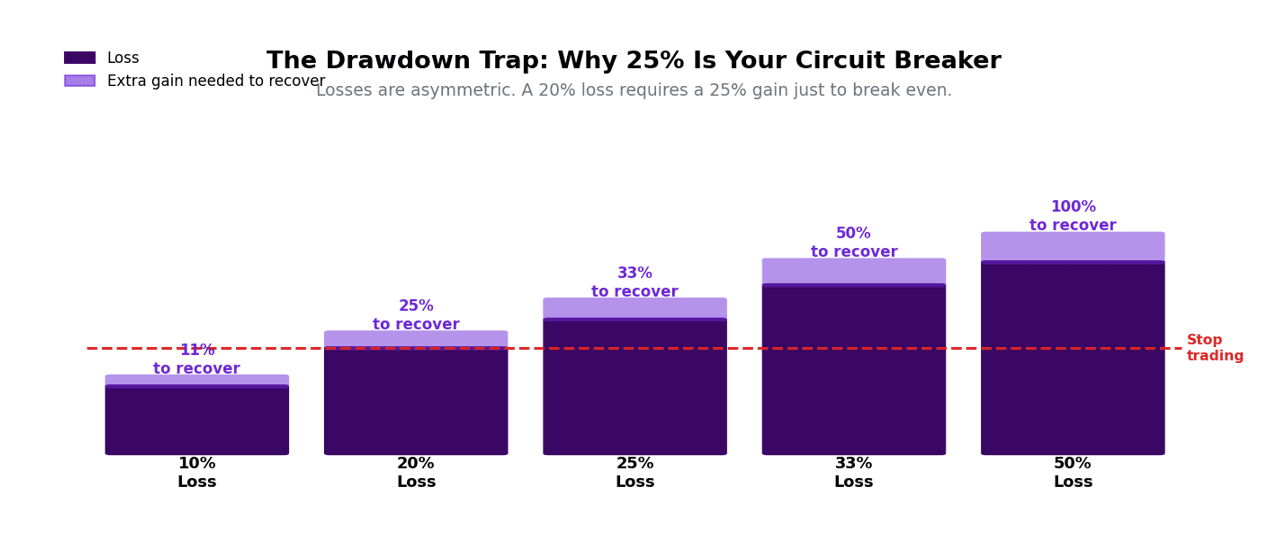

The Drawdown Rule: When to Stop Trading and Why It Matters

Define your circuit breaker before you need it. Most serious traders pause at 20 to 25% drawdown. With a $2,000 bankroll, that means stopping when your balance hits $1,500, stepping back, reviewing your process, and only resuming after identifying what went wrong.

Why 20 to 25% is the threshold: Mathematically, you need a 25% gain to recover from a 20% loss, and a 33% gain to recover from a 25% loss. Drawdowns beyond 25% require increasingly unlikely winning streaks to return to breakeven, and the psychological weight destroys discipline faster than any losing streak.

What to do when you hit your drawdown limit

Stop all new positions immediately

Let existing positions resolve. Do not panic close for losses

Review your last 20 trades for sizing errors, not just outcome errors

Identify if losses came from bad luck or bad process

Return at original unit size only. Never increase size to win it back faster

The traders who blow up prediction market accounts are almost never the ones who picked too many wrong outcomes.

They are the ones who kept increasing size trying to recover losses. Chasing losses with bigger positions is the fastest path to zero. |

Bankroll Management by Trader Profile

Different trading styles demand different position sizing approaches.

| Trader Type | Trades/Month | Method | Max Per Trade | Max Concurrent |

|---|---|---|---|---|

| Casual | 5–10 | Fixed 2% | $40 on $2K | 5 |

| Active | 50+ | Quarter Kelly | Varies by edge | 10–15 |

| Arbitrage | 20–40 pairs | Flat dollar | $100–500 per pair | 3–5 pairs |

Why arbitrage traders use flat dollar sizing: Arbitrage edge is defined by the spread between platforms, not by a probability estimate. If Polymarket shows 58c and Kalshi shows 54c, you know your exact 4c edge. Kelly criterion does not apply cleanly because there is no probability estimation, just math. Arbitrage traders set position sizes based on available liquidity and capital efficiency.

Frequently Asked Questions

What percentage of my bankroll should I risk per trade?

Two to five percent per trade is the standard range for active traders. Start at 2% until you have 50 or more resolved trades to evaluate your actual edge, then adjust upward only if your win rate and expected value justify it. Never exceed 5% on a single position regardless of confidence.

Does Kelly criterion work for prediction markets?

Yes, but use Quarter Kelly rather than Full Kelly. Full Kelly maximizes long-run growth but produces drawdowns of 30 to 50% that most traders cannot hold through emotionally. Quarter Kelly gives roughly 75% of the growth with far more manageable variance.

How many prediction markets should I have open at once?

Ten to fifteen for an active trader with a $2,000+ bankroll, provided no more than three or four are correlated. For a $500 bankroll, five concurrent positions is the practical ceiling before a single correlated event can cause a damaging drawdown.

What should I do after a big losing streak?

Stop trading when you hit your pre-defined drawdown threshold of 20 to 25% of starting bankroll. Review your last 20 trades for sizing errors, not just outcome errors. Do not increase position size to recover losses faster. Return at your original unit size only after identifying process failures.

Is bankroll management different on Polymarket vs Kalshi?

The sizing framework is identical. The difference is fee drag: Polymarket charges lower taker fees on most markets, which means your edge threshold per trade is slightly lower. On Kalshi's fee-enabled markets your position needs to carry more expected value to justify the same dollar risk.

The Three Non-Negotiable Rules1. Define your bankroll and never touch it mid-cycle. 2. Pick your sizing method and stick to it regardless of recent results. 3. Set your drawdown circuit breaker before you need it. Good sizing does not guarantee profits. It keeps you in the game long enough for your edge to compound over hundreds of trades instead of blowing up on trade seventeen. |

Disclaimer: This article is for educational purposes only and does not constitute financial or investment advice. Prediction market trading involves significant risk. Always conduct your own research before committing capital.