Traditional financial markets price geopolitical risk imprecisely. When a geopolitical event escalates, equity markets sell off, oil spikes, and safe-haven assets attract flows, but the magnitude and direction of these moves reflect sentiment and positioning rather than calibrated probability assessments of specific outcomes. A prediction market geopolitical hedge works differently. Instead of buying volatility or selling risk assets to protect a portfolio, you buy a contract on the specific outcome you are worried about at an explicitly stated probability price. If that outcome occurs and your portfolio suffers, the contract pays $1 per share. If the outcome does not occur and your portfolio is fine, you lose the premium you paid for the hedge.

That structure makes prediction markets genuinely useful as portfolio insurance against specific tail risks in a way that traditional financial hedging instruments are not. A VIX call does not tell you the probability of a US-Iran military confrontation. A prediction market contract does. And a position in that contract pays off precisely when the event you feared actually happens, not merely when markets become more volatile.

This guide covers which geopolitical events are priced on Polymarket and Kalshi, how those prices compare to the assessment of structured geopolitical risk frameworks, how to build a practical hedging framework around prediction market positions, and the specific sizing and liquidity constraints that matter before implementing this approach. For the foundational mechanics of how prediction market prices work as probability estimates, Polymarket explained: how prediction markets work covers the complete structure before going into hedging-specific applications.

Why Geopolitical Events Create Portfolio Risk That Traditional Hedging Misses

The standard toolkit for hedging portfolio risk against geopolitical events relies on instruments that are correlated with risk sentiment rather than specific outcomes. Buying gold, selling equity index futures, buying VIX calls, or holding cash all provide protection against broad market volatility but do not pay off specifically when the event you are worried about occurs.

This creates two problems. First, the hedge may not pay off when you need it. A geopolitical escalation that markets have already partially priced produces a smaller VIX spike and a smaller gold rally than an event that comes as a complete surprise. If you are hedging against an event that markets are already partially pricing, your standard hedging instruments are already partially expensive and will partially underperform when the event occurs.

Second, the hedge will pay off when you do not need it. Broad market volatility can spike for reasons that have nothing to do with the specific geopolitical risk you are trying to hedge. A VIX call that you bought as Russia-Ukraine insurance may pay off because of a Federal Reserve surprise rather than because of an escalation in Eastern Europe. In that scenario, your hedge paid off but your underlying geopolitical exposure was not actually triggered.

A geopolitical risk prediction market position solves both problems. It pays off only when the specific event you identified occurs. It does not pay off because of unrelated volatility. And the price you pay reflects the market's assessed probability of that specific outcome, making it possible to calculate whether the hedge is fairly priced relative to the risk it covers.

Which Geopolitical Events Are Tradeable on Polymarket

The range of geopolitical events covered by Polymarket and Kalshi as of 2026 is broad enough to cover the most common categories of portfolio-relevant geopolitical tail risk.

War and military conflict markets

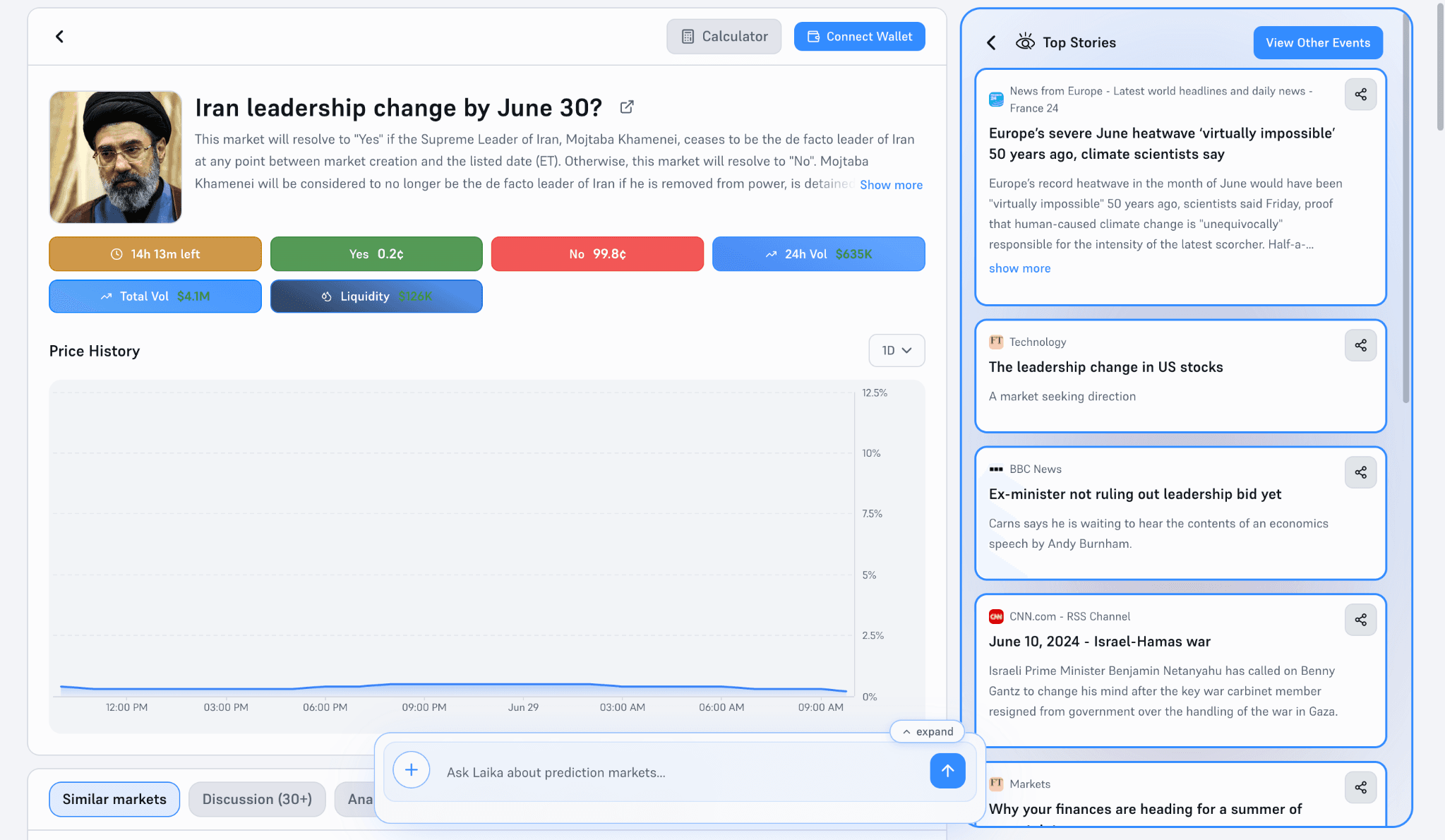

Military conflict markets are the most directly relevant to portfolio hedging because they represent the highest-impact geopolitical tail risks for most asset portfolios. Polymarket has run active markets on US-Iran military confrontation probability, Russia-Ukraine ceasefire and escalation scenarios, Israel-Hamas conflict duration and resolution, North Korea missile testing and nuclear escalation, and China-Taiwan tension scenarios.

These markets price outcomes that financial market instruments cannot price directly. An oil portfolio that is specifically exposed to a US-Iran military confrontation in the Strait of Hormuz can be hedged with a YES position on the US-Iran conflict market in a way that a crude oil futures position or a geopolitical ETF cannot replicate. The contract pays off specifically when the event that damages the portfolio occurs, which is the correct structure for a hedge.

For the specific analytical framework for trading Iranian conflict risk markets including how to assess the reliability of the underlying probability estimates, Iran war markets on Polymarket: what traders need to know covers the methodology in detail.

Sanctions and trade policy markets

Polymarket runs markets on specific sanctions implementations, trade tariff decisions, and export control changes that directly affect equity portfolios with concentrated exposure to affected sectors or geographies. Semiconductor companies exposed to China export controls, energy companies exposed to Russian sanctions regimes, and financial institutions exposed to Iranian sanctions compliance risk all face specific policy outcomes that are priced on Polymarket before they are reflected in equity prices.

A technology portfolio with concentrated exposure to companies affected by US-China semiconductor export controls can take YES positions on specific export control tightening markets. If the controls tighten and the portfolio suffers, the contract pays off. If the controls do not tighten, the portfolio is fine and you lose the small premium paid for the protection.

Government shutdown and fiscal cliff markets

US government shutdown markets represent a specific category of geopolitical risk that is directly portfolio-relevant for fixed income investors, defense contractors, federal contractors, and any portfolio with concentrated exposure to government spending. Shutdown probabilities are actively traded on Polymarket and have historically shown significant divergence from equity market pricing of the same risk during the weeks leading up to shutdown deadlines.

For the specific framework for trading government shutdown risk markets, US government shutdown markets: how to trade political gridlock covers the approach in detail.

Election outcome markets

Election outcome markets represent the most liquid category of politically relevant prediction market contracts and are directly applicable as hedging instruments for portfolios that have asymmetric exposure to specific electoral outcomes. A portfolio that would be significantly harmed by a specific party winning a specific election can take a YES position on that outcome as a direct portfolio hedge.

The 2026 midterm markets are the most immediately relevant for US-based portfolios. Congressional control markets price the probability of specific legislative outcomes that affect sector-level equity exposure in healthcare, energy, financial services, and technology.

A Practical Hedging Framework Using Prediction Market Positions

Building a portfolio insurance strategy around prediction market positions requires four analytical steps that are different from the steps required for directional trading.

Step 1: Identify the specific geopolitical outcomes that would materially harm your portfolio

Most investment portfolios have concentrated exposure to specific geopolitical tail risks rather than generic geopolitical volatility. A global equity portfolio may have concentrated exposure to Taiwan semiconductor supply chains. An emerging market portfolio may have concentrated exposure to Russian energy sanctions. A technology portfolio may have concentrated exposure to US-China technology decoupling.

The first step is identifying which specific events would cause material harm to your portfolio and quantifying the approximate magnitude of that harm. If a US-Iran military confrontation that closes the Strait of Hormuz would reduce your oil-exposed portfolio by 15 to 20 percent, you have identified a specific hedgeable risk with a quantifiable magnitude.

Step 2: Find the corresponding prediction market contract and assess its price

Once you have identified the specific risk event, find the prediction market contract that most closely prices that event. Compare the contract's implied probability to your own assessment of the event's likelihood and to structured geopolitical risk assessments from frameworks like those published by the Council on Foreign Relations risk tracker at cfr.org.

If the prediction market prices a US-Iran military confrontation at 12% and your own assessment is 18 to 20%, the contract is cheap relative to your risk assessment. That is a favorable hedging price. If the contract is at 25% and your assessment is 15%, the contract is expensive relative to your view and the hedge is not cost-effective at the current price.

This comparison is the step that most pure trading frameworks skip because they focus on edge rather than insurance value. For a hedge, you do not need to believe the contract is mispriced in your favor. You need to assess whether the premium you pay for the protection is justified by the magnitude of the portfolio loss it covers.

Step 3: Size the position to provide meaningful protection relative to the portfolio risk

Prediction market hedging positions should be sized relative to the portfolio loss you are trying to protect against, not relative to a conventional prediction market position sizing framework. The correct question is not how much of my trading budget should I allocate to this contract but how much protection do I need against this specific outcome.

A simplified sizing framework: if a 12% probability event would cause a $10,000 loss in your portfolio, and you want 50 percent coverage of that expected loss, you need a prediction market position that pays $5,000 if the event occurs. At a contract price of $0.12, that requires approximately $600 in premium to purchase 5,000 shares that pay $5,000 at $1 each if the contract resolves YES.

The $600 premium represents 6 percent of the $10,000 potential loss you are protecting against. Whether that premium is acceptable as portfolio insurance depends on your assessment of the event probability, the magnitude of the loss you are protecting, and the availability of alternative hedging instruments.

Step 4: Monitor the position as the geopolitical situation evolves

Unlike a traditional options hedge that decays over time regardless of what happens in the world, a prediction market hedge gains or loses value based on the evolving probability of the specific event you have hedged against. If the geopolitical situation escalates and the underlying risk increases, the prediction market contract price rises and your hedge position gains value before the event has even occurred.

This real-time mark-to-market feature of prediction market hedges creates a specific opportunity that traditional hedging instruments do not offer. When a geopolitical situation is escalating and your hedge position has moved from $0.12 to $0.28, you have three choices: sell the position and realize a hedging profit that partially offsets the paper losses in your underlying portfolio that escalation has already caused, hold the position for further upside if the escalation continues, or add to the position if the risk-adjusted premium at the new price still justifies the protection.

For how prediction market positions correlate with cryptocurrency portfolios specifically and how to build hedges that account for crypto-specific geopolitical risk factors, crypto correlation trading with prediction markets covers the framework.

Sizing and Risk Limits for Prediction Market Portfolio Insurance

Prediction market portfolio insurance has specific constraints that differ from traditional hedging instruments and that require explicit risk management frameworks before implementation.

The liquidity constraint

The most significant practical constraint on prediction market hedging is order book depth. A large equity portfolio that needs $50,000 in geopolitical hedge protection may find that the prediction market contract on the relevant event cannot absorb a $50,000 position without significant slippage that reduces the effective hedge ratio.

Check order book depth before sizing any prediction market hedge above $5,000 on a single contract. War and conflict markets during active escalation periods are the most liquid geopolitical contracts, sometimes reaching $5 to $10 million in volume. The same markets during quiet periods may have $200,000 in total volume, which limits meaningful position sizing.

The correlation assessment

Before implementing a prediction market hedge, assess whether the contract is actually correlated with your portfolio loss in the way you expect. A US-Iran conflict market that pays off when a military confrontation occurs is a good hedge for a portfolio with Strait of Hormuz oil exposure. It is a poor hedge for a technology portfolio that would be harmed by a completely different aspect of Middle East tension.

Map the specific mechanism by which the geopolitical event damages your portfolio before assuming the prediction market contract is the right hedge instrument. The payment trigger on the contract must match the damage trigger on the portfolio.

The timing mismatch risk

Prediction market contracts resolve on specific dates or when specific events are confirmed. Your portfolio loss may crystallize before or after the contract resolves. A defense contractor portfolio that loses value because of escalating China-Taiwan tensions may suffer losses before a specific Polymarket contract on military conflict resolves, because equity markets price the increasing probability of conflict before the conflict itself occurs.

This timing mismatch means prediction market hedges work best as protection against the actual occurrence of the event rather than as protection against the market's increasing pricing of event probability. If you want protection against increasing geopolitical risk pricing in financial markets rather than the actual event, traditional volatility instruments are more appropriate than prediction market contracts.

The premium management framework

Prediction market hedging premiums should be budgeted annually as a cost of portfolio risk management rather than as a one-time expense. A systematic geopolitical hedging program might allocate 0.5 to 1.5 percent of portfolio value annually to predict market insurance premiums across a diversified set of geopolitical tail risks. That allocation should be reviewed quarterly as the geopolitical environment changes and new markets become available.

For the complete framework on position sizing across multiple prediction market categories including how to budget across simultaneous geopolitical hedging positions, the prediction market bankroll management guide covers the methodology.

Frequently Asked Questions

Can you use prediction markets to hedge geopolitical risk?

Yes, with specific limitations. Prediction market contracts on war, sanctions, election outcomes, and policy changes can provide direct portfolio insurance against specific geopolitical outcomes. The contract pays $1 per share if the event occurs, which directly offsets the portfolio loss if your underlying assets are damaged by that event. The primary limitations are order book depth, which constrains position sizing, and the timing mismatch between contract resolution and portfolio mark-to-market, which means the hedge works best against the actual event rather than against increasing event probability in financial markets.

Which geopolitical events are tradeable on Polymarket?

Polymarket currently hosts active markets on US-Iran military confrontation probability, Russia-Ukraine conflict and ceasefire scenarios, Israel-Hamas conflict duration, China-Taiwan tension escalation, North Korea nuclear risk, US government shutdown probability, and a range of election outcome markets across major global economies. The availability and liquidity of specific contracts changes with the geopolitical news cycle. Check the current active markets at polymarket.com for the live geopolitical contract menu.

How do prediction markets price war and conflict risk?

War and conflict markets on Polymarket are priced by the aggregate of all capital-backed trader positions on the platform's central order book. Prices reflect the crowd's assessment of escalation probability given available public information including diplomatic communications, military positioning data, and historical base rates for conflict escalation. Prediction market prices on conflict risk have been shown to track structured geopolitical risk assessments from organizations like the Council on Foreign Relations reasonably closely, though they update in real time while institutional assessments update on a quarterly or annual basis.

What is the best way to use Polymarket as portfolio insurance?

The most effective framework identifies the specific geopolitical events that would materially harm your portfolio, finds the Polymarket contract that most directly prices that event, compares the contract price to your own probability assessment to determine whether the hedge premium is justified, sizes the position based on the magnitude of the loss you are protecting against rather than on conventional trading position sizing, and monitors the position actively as the geopolitical situation evolves. Limit individual hedge positions to markets with sufficient order book depth to absorb your target position size without significant slippage.

Where can I find discussion on geopolitical hedging with prediction markets?

The prediction markets subreddit on Reddit carries active discussion of geopolitical event markets including specific hedging applications during escalation periods. On geopolitical prediction market reddit threads, the most useful discussions tend to appear during active escalation periods when volume and community attention concentrate on the specific risk events being priced. The Polymarket Discord communities focused on political and geopolitical markets also carry analytical discussion of specific contract pricing relative to structured risk assessments.

The Bottom Line

Prediction market portfolio insurance occupies a specific and underused space in the geopolitical risk management toolkit. It provides protection that pays off specifically when the event you fear occurs, at a price that reflects an explicitly stated probability rather than the opaque risk premium embedded in traditional hedging instruments.

The framework is not a replacement for traditional portfolio risk management. It is a complement to it that covers the specific scenario where you want protection against a named, probability-priced geopolitical outcome rather than against generic volatility. A conflict escalation market that is priced at 12% and would cause a 15% drawdown in your portfolio represents a specific, manageable, hedgeable risk that prediction markets price more cleanly than any alternative instrument.

The constraints are real: order book depth limits position sizing, timing mismatches reduce hedge effectiveness against probability changes rather than actual events, and the premium must be evaluated against the magnitude of the risk being covered. Within those constraints, systematic geopolitical hedging using prediction market positions is one of the most direct and cost-effective portfolio insurance tools available to active investors in 2026.

Track how geopolitical event probabilities move in real time across every active Polymarket contract with Polymetric by Laika AI. Live market intelligence for investors who want to see geopolitical risk repricing before it reaches financial markets.