The data is brutal and unambiguous. Analysis of over 50,000 Polymarket wallets shows that only 7.6% achieve any profitability after fees. When you filter for sustained profitability over six months or more, that number drops to approximately 3%.

This means 97 out of every 100 people who trade on Polymarket lose money. Not break even. Not achieve modest returns. They lose capital.

The difference between the 3% who profit and the 97% who lose is not access to secret information. Both groups read the same news. Both see the same markets. Both have access to the same data sources.

The difference is psychology. How they think about uncertainty. How they handle being wrong. How they size positions. How they interpret information. How they manage emotions when markets move against them.

This article breaks down the specific cognitive patterns that separate profitable traders from everyone else, the emotional traps that destroy accounts, the decision-making frameworks winners use consistently, and the mental models that turn prediction market trading from gambling into systematic edge extraction.

The Fundamental Psychological Divide

Profitable traders and unprofitable traders approach Polymarket from completely different mental frameworks.

Unprofitable traders think in certainties

The losing trader looks at a presidential election market showing 65 cents and thinks: "Candidate X is obviously going to win. This is free money."

They are expressing certainty about an uncertain future. They have converted a probabilistic event into a binary prediction. In their mind, there is a correct answer and the market has it wrong.

This mindset is fatal because prediction markets are not about being right or wrong. They are about being more right than the current price more often than you are wrong.

When the losing trader's "certain" outcome fails to occur, they experience it as a shocking betrayal of reality rather than as a normal outcome within a probability distribution.

Profitable traders think in probabilities

The winning trader looks at the same 65-cent market and thinks: "The market is pricing this at 65% probability. Based on my analysis of polls, early vote data, and historical patterns, I estimate the true probability at 71%. That 6-point edge justifies a position."

They are not predicting certainty. They are estimating probability and comparing it to market pricing. They understand that even at 71% true probability, this outcome fails to occur 29% of the time, and that is completely normal.

When their position loses, they do not experience shock. They update their model and ask whether their probability estimate was wrong or whether they just experienced normal variance.

This is the foundational divide. Certainty thinking versus probabilistic thinking. Everything else flows from this.

Why certainty thinking dominates

Human brains evolved for a world of immediate physical threats, not for probabilistic reasoning about abstract future events. Our neural architecture is built for: see tiger, run from tiger, survive. Not for: aggregate polling data, adjust for historical error, estimate probability distribution.

Certainty feels good. Saying "X will definitely happen" is emotionally satisfying. It eliminates anxiety. It makes you feel smart and informed.

Probability thinking feels uncomfortable. Saying "I estimate 68% probability with a confidence interval of plus or minus 7 points" feels weak. It leaves room for being wrong. It requires intellectual humility.

Most traders choose the cognitive mode that feels good rather than the mode that makes money.

Emotional Control Separating Winners from Losers

Trading psychology research consistently shows that emotional regulation predicts trading success better than intelligence, education, or experience.

The revenge trading trap

Losing traders experience this pattern constantly:

- Place a position based on analysis

- Position goes underwater immediately

- Feel stupid and angry

- Place a larger position on another market to make money back quickly

- That position also loses

- Feel more desperate

- Place even larger position

- Account blown up within days

This is revenge trading. The emotional need to recover losses quickly overrides systematic decision-making. Each loss increases emotional pressure, which degrades judgment further, creating a death spiral.

How profitable traders handle losses

Winning traders experience losses constantly. A 65% win rate means 35% of positions lose. The difference is they have systematic responses to losses rather than emotional reactions.

When a position loses, the profitable trader asks:

- Was my analysis wrong or did normal variance occur?

- What new information emerged that I did not account for?

- Should I update my model based on this outcome?

- What is the next highest-edge opportunity available?

They do not ask:

- How can I make this money back immediately?

- Which market can I bet bigger on to recover?

- Why does this always happen to me?

The profitable trader treats each loss as information. The unprofitable trader treats each loss as an injustice requiring revenge.

Position sizing as emotional regulation

Winning traders size positions to stay emotionally stable. If a $5,000 loss would cause you to spiral into revenge trading, your maximum position size is much smaller than $5,000.

Most losing traders size positions based on how confident they feel about the outcome. High confidence equals large position. This is backwards.

Confidence is a feeling, not a probability estimate. You should size positions based on edge and risk tolerance, not based on how certain you feel.

The formula is simple: if a loss would cause you emotional distress that degrades your decision-making, the position is too large regardless of your conviction level.

The euphoria trap

Winning trades create their own psychological danger. A trader who wins three positions in a row starts to feel invincible. They increase position sizes. They enter marginal trades they would have skipped when cautious. They stop doing research because their "hot hand" will carry them.

Then they lose. The larger position size creates a larger loss. The marginal trades they entered have negative expectations. The research they skipped would have revealed information that invalidated the trade.

Profitable traders treat winning streaks as variance requiring caution, not as proof of skill requiring larger bets. They know that three wins in a row is not statistically meaningful. They maintain consistent position sizing and analysis rigor regardless of recent results.

Information Processing That Creates Edge

Both profitable and unprofitable traders have access to the same information. The difference is what they do with it.

Confirmation bias is the silent killer

Unprofitable traders decide what they believe will happen, then seek information confirming that belief while ignoring contradictory information.

Example: Trader believes Candidate X will win the election. They read polls showing X ahead and think "see, I was right." They read polls showing X behind and think "that pollster is biased" or "this is an outlier."

They are not analyzing information. They are defending a pre-existing belief.

Profitable traders actively seek information that contradicts their position. If they own YES in a market, they specifically look for reasons NO might win. This sounds counterintuitive but it prevents the catastrophic losses that occur when contradictory information you ignored all along proves decisive.

Base rate neglect destroys accounts

Unprofitable traders focus on the specific narrative of each market while ignoring base rates.

Example: A challenger candidate has an inspiring story, strong fundraising, and good debate performance. The trader thinks "this candidate will pull an upset" and buys the challenger at 35 cents.

What they ignored: challengers win only 18% of races in this type of district historically. Even with favorable specific factors, the base rate probability is low. The market price of 35 cents might already be generous.

Profitable traders start with base rates and adjust based on specific information. They ask: what happens in situations like this historically? Then they adjust that baseline up or down based on specific factors unique to this case.

Starting with the specific story and ignoring the base rate is how traders convince themselves that 30% probability events will "definitely happen."

Recency bias and availability heuristic

Recent events dominate memory more than distant events. Dramatic events dominate memory more than boring events. This creates predictable errors.

If a candidate had a strong debate performance last night, unprofitable traders overweight that single event. If a recent poll showed a dramatic shift, they assume the trend will continue.

Profitable traders track information over time. One debate matters less than six months of polling trends. One dramatic event matters less than systematic patterns.

They also recognize when the market is overweighting recent information. If a market moves 15 cents on one debate performance, and historical analysis shows debate performances rarely change outcomes by more than 2-3 points, the market has overreacted. That overreaction is an edge opportunity.

Analysis paralysis versus premature action

There is a zone between doing too little research and doing too much.

Unprofitable traders fall into both traps. Some do almost no research, trading based on headlines and gut feelings. Others do endless research, reading every article and analyzing every data point until they have lost the timing edge.

Profitable traders have systematic research processes. They identify the three to five factors that matter most for each market category. They research those factors thoroughly. Then they decide.

For political markets: polling averages, early vote data, historical comparisons, pollster quality, and demographic trends. Research those five factors. Make a decision. Do not spend six hours reading opinion pieces that add no new information.

For economic markets: Fed speeches, economic data trends, market expectations (CME Fed futures), historical Fed behavior, and institutional forecasts. Research those. Decide.

Having a systematic process prevents both doing too little research (missing critical information) and doing too much research (missing timing while the edge disappears).

Cognitive Biases That Separate Winners and Losers

Everyone experiences cognitive biases. Profitable traders have systems that compensate for biases. Unprofitable traders let biases drive decisions.

Overconfidence is the biggest killer

Humans are systematically overconfident about their knowledge and abilities. 80% of drivers think they are above average. Most traders think they are smarter than the market.

Overconfidence causes traders to:

- Size positions too large relative to actual edge

- Enter trades without sufficient research

- Ignore contradictory information

- Fail to use stop losses because they "know" they are right

- Overtrade because they think they have edge in more markets than they actually do

Profitable traders combat overconfidence by tracking performance religiously. When you have a spreadsheet showing your actual win rate is 58%, not the 75% you assumed, it forces calibration.

They also use pre-commitment devices. Before placing a trade, they write down: my probability estimate is X, market price is Y, I am risking Z amount, I will exit if price reaches W or if information Q emerges.

Writing it down and tracking whether estimates were accurate calibrates confidence over time.

Loss aversion creates asymmetric decisions

Loss aversion is the psychological reality that losses hurt roughly twice as much as equivalent gains feel good.

This causes predictable errors:

- Holding losing positions too long because selling makes the loss real

- Selling winning positions too quickly to lock in the good feeling

- Avoiding good trades with moderate edge because the possibility of loss feels too painful

Profitable traders recognize loss aversion and actively compensate. They force themselves to take losses at predefined exit points even though it hurts. They hold winning positions until their predefined profit target even though selling early would feel good.

They understand that making 10 bets with 60% win rate and proper risk management will produce positive returns even though it means enduring four painful losses out of every ten bets. Avoiding that pain means avoiding the entire strategy that generates long-term profit.

Sunk cost fallacy kills accounts

Unprofitable traders frequently think: "I have already lost $2,000 on this position. I need to hold it to make that money back."

This is a sunk cost fallacy. The $2,000 is gone. The only question that matters is: given current information and current prices, is this position a positive expectation going forward?

If the answer is no, exit immediately. The amount you have already lost is irrelevant to whether you should continue holding.

Profitable traders treat every moment as a fresh decision. Am I getting good odds right now? If yes, hold. If no, exit. What happened in the past is data for learning but not a reason to hold bad positions.

Anchoring to first information received

Humans anchor to the first number they see. If you see a market priced at 70 cents, then do research, your probability estimate tends to stay close to 70 cents even if research suggests 55 cents or 85 cents.

Unprofitable traders anchor to initial market prices or to their first impression of an event.

Profitable traders deliberately resist anchoring by:

- Forming independent estimates before looking at market prices

- Asking "if this market was priced at 30 cents or 90 cents, would my analysis be different?"

- Checking whether their probability estimate is unreasonably close to the current market price (suggesting unconscious anchoring)

If you estimate 69% probability and the market is 68 cents, be suspicious. You might have unconsciously anchored to market price rather than forming an independent estimate.

If you cannot articulate specifically why your analysis is better than the current market price, you do not have an edge. Do not place the trade.

Treat each trade as one instance in a distribution

The biggest mental model difference between profitable and unprofitable traders is how they conceptualize individual trades.

Unprofitable traders see: this trade will win or lose.

Profitable traders see: this trade is one draw from a probability distribution. I am estimating that distribution better than the market. Some draws will win, some will lose. I make positive returns by having better distribution estimates repeated across many draws.

This mental model eliminates the emotional volatility of winning and losing streaks. Three wins in a row is not "I am a genius." Three losses in a row is not "I am terrible at this." Both are normal variance in distributions where probability is neither 0% nor 100%.

When you internalize this model, losing trades stop creating emotional spirals because you expect a percentage of trades to lose from the beginning.

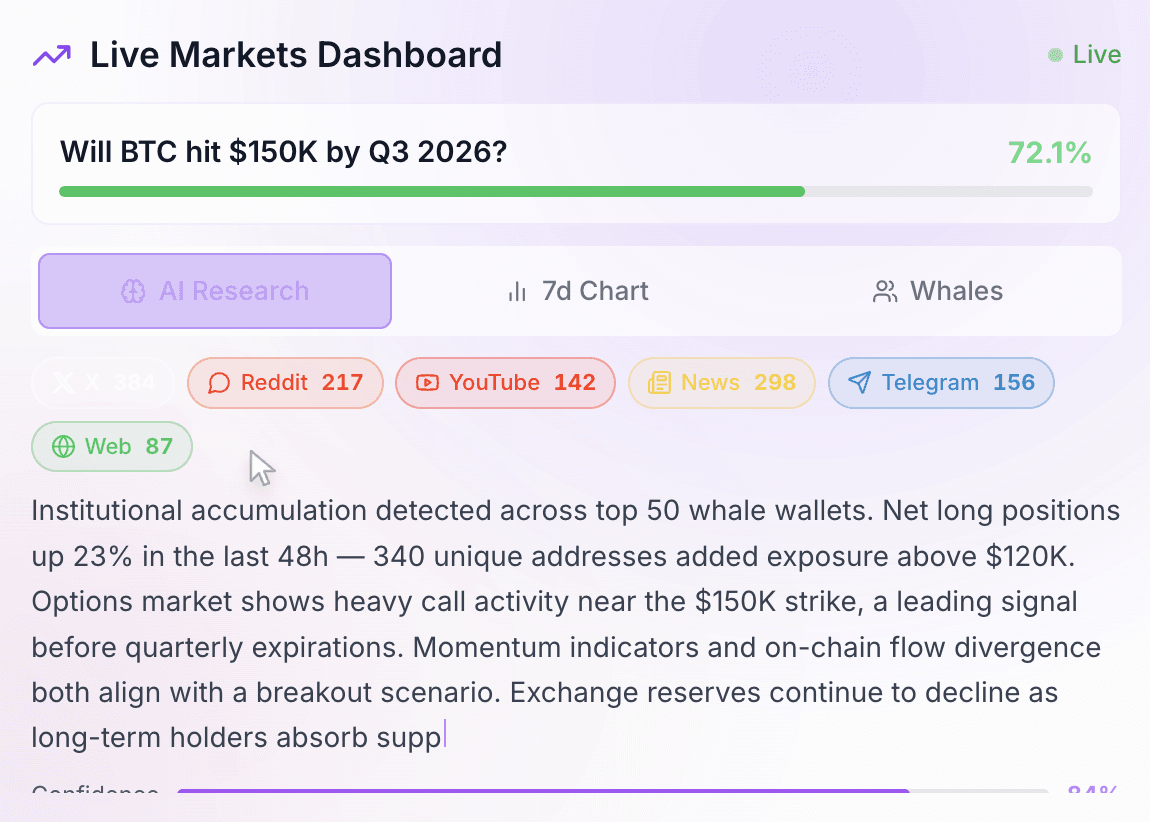

Using Laika AI for systematic research

Laika AI helps traders avoid psychological traps by systematizing the information gathering process.

Instead of selectively reading articles that confirm your existing beliefs (confirmation bias), Laika aggregates news across multiple sources and surfaces information you might have missed.

Instead of overweighting recent dramatic events (recency bias), Laika provides historical context and comparable situations.

Instead of making decisions based on gut feelings, Laika's whale tracking shows what historically successful traders are doing, providing a reality check on whether your analysis aligns with sophisticated market participants or conflicts with them.

The psychology benefit is not that Laika makes decisions for you. It is that systematic information gathering prevents the selective attention and confirmation bias that destroy accounts.

Frequently Asked Questions

What percentage of Polymarket traders are profitable?

Approximately 7.6% of Polymarket wallets show any profitability after fees based on analysis of over 50,000 wallets. When filtering for sustained profitability over six months or longer, that number drops to roughly 3%. This means 97% of participants lose money over time.

Why do most Polymarket traders lose money?

Most traders lose because of psychological errors rather than information disadvantages. They think in certainties rather than probabilities, size positions emotionally rather than systematically, fall victim to confirmation bias and overconfidence, revenge trade after losses, and lack systematic decision-making processes. They also overtrade outside their circle of competence.

How do profitable traders think differently about probability?

Profitable traders think in probability distributions rather than binary outcomes. They estimate percentage probabilities, compare to market pricing, identify edges, and accept that even high-probability outcomes fail regularly. They judge trades by decision quality not outcomes, understanding that good trades lose 30-40% of the time in probabilistic environments.

How do I avoid confirmation bias when researching markets?

Actively seek information contradicting your position. If you own YES, deliberately look for reasons NO might win. Review your research process in your trading journal. Use systematic information gathering tools like Laika AI that aggregate multiple sources rather than selectively reading articles you agree with.

What is expected value thinking in Polymarket trading?

Expected value thinking means evaluating trades by probability times payoff across many repetitions rather than trying to win each individual bet. A 60% probability trade will lose 40% of the time, which is normal. You profit by making positive expected value decisions repeatedly, accepting that many individual instances will lose.

Can Laika AI help with Polymarket trading psychology?

Laika AI helps prevent psychological errors by systematizing information gathering, reducing confirmation bias through multi-source aggregation, providing historical context that combats recency bias, and showing whale trader positioning as a reality check against overconfidence. The platform does not make decisions for you but creates systematic research workflows that prevent emotional and cognitive errors.