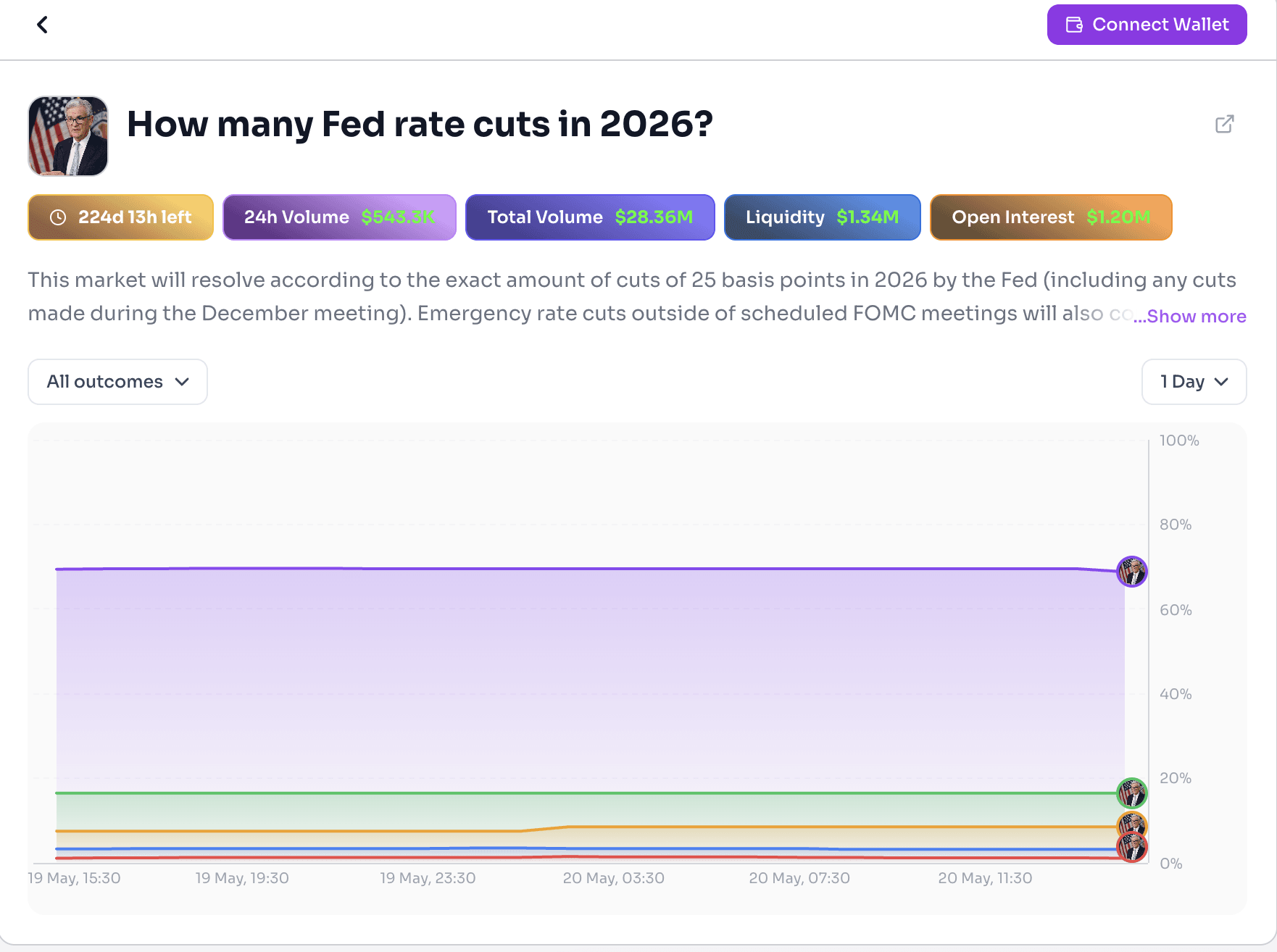

The Polymarket market on Federal Reserve rate cuts in 2026 is one of the most actively watched economic contracts on the platform right now. As of now it has $28.36 million in total volume, $1.34 million in liquidity, $1.20 million in open interest, and 224 days remaining until resolution on December 31, 2026.

The chart from the screenshot tells the whole story at a glance. The purple line, representing zero cuts, is sitting above 60% and has barely moved in the past 24 hours. The green line representing one cut sits around 20%. Two cuts at roughly 10%. Three or more cuts are barely visible above zero

Current Polymarket Odds

Why Zero Cuts Is Dominant: 3 Reasons

- April 2026 CPI hit 3.8% year-over-year. Highest reading since May 2023. Driven by a 17.9% energy price surge tied to the Iran conflict. The Fed cannot credibly cut rates when inflation is running this hot.

- Three consecutive holds already in 2026. January, March, and April 29 all produced holds at 3.50% to 3.75%. CME FedWatch currently prices June 17 to 18 at 99.9% hold probability. That is not a slight lean toward holding. That is a near-certainty.

- New Fed Chair credibility dynamic. Jerome Powell's term expired May 15, 2026. Any incoming Chair who cuts rates within their first months in office while CPI is at 3.4% or higher faces immediate bond market credibility damage. The institutional incentive is to hold, not cut.

Remaining 2026 FOMC Meeting Calendar

The Case FOR One Cut: 4 Catalysts to Watch

- May CPI release on June 10 is the first major data point. If energy prices reverse on Iran ceasefire continuation, headline CPI could drop from 3.8% toward 3.2% to 3.3%. That changes the Fed's arithmetic significantly.

- The FOMC's own March 2026 dot plot projected a single rate cut in 2026 as the median member expectation. That institutional signal has not been officially abandoned. The Fed itself was leaning toward one cut before the Iran energy spike.

- Labour market softening in August or September jobs reports would give the Fed dual mandate justification to act. Current unemployment is 4.3%. A move toward 4.6% to 4.8% combined with lower inflation is the classic setup for a late-year single cut.

- New Chair positioning. Once settled in office, iShares and other institutional forecasters project the new Chair may seek one or two cuts toward 3.00% to 3.25% in the second half of the year, assuming the data cooperates.

The Case AGAINST Any Cut: 4 Structural Barriers

- Sticky non-energy inflation. Shelter costs and services inflation are resistant to rate hikes already implemented. One energy price reversal does not fix the underlying inflation structure.

- New Chair credibility incentive. First months in office are the worst time to deliver rate cuts when inflation is above target. Markets would interpret it as political pressure rather than data-driven policy.

- The labour market remains too strong. Unemployment at 4.3% with steady payroll gains does not give the Fed a recession risk pretext. Cuts need either inflation clearly broken or growth clearly broken. Neither condition is currently met.

- CME FedWatch institutional consensus. Professional futures traders are pricing 77.5% probability the Fed stays on hold through all of 2026. Polymarket at 70% for zero cuts is actually slightly more dovish than the institutional market, meaning the institutional market is even more bearish on cuts than Polymarket currently reflects.

Institutional Forecasts vs. Polymarket

The key observation from this table: Polymarket is slightly more optimistic about rate cuts than the institutional futures market. The zero cuts outcome at 68% to 70% on Polymarket against 77.5% on CME FedWatch creates a small but measurable divergence worth noting.

How This Market Resolves

- Resolution date is December 31, 2026 at 11:59 PM ET.

- Resolution source is the official Federal Reserve website at federalreserve.gov.

- Emergency cuts outside scheduled meetings count toward the total.

- A single 50 bps cut counts as two separate 25 bps cuts.

- If the Fed makes two cuts by October, zero cuts and one cut contracts immediately resolve to zero and pay nothing.

- The market can resolve early for any outcome that becomes mathematically impossible before year end.

Frequently Asked Questions

Why is zero cuts the dominant outcome on Polymarket?

April 2026 CPI hit 3.8% year-over-year too hot for near-term cuts. Three consecutive holds in 2026 have already set a clear trajectory, and the new Fed Chair has every incentive to hold firm on inflation before considering any easing.

Is the one cut outcome at 18–20% a value bet?

Possibly. The FOMC's own March 2026 dot plot projected one cut this year — before the Iran energy spike. If that inflation proves temporary, one cut is pricing a scenario the Fed itself was planning just two months ago.

What is the most important upcoming data release?

The May CPI print on June 10. A big downside surprise shifts cut odds higher immediately; a reading above 3.5% locks in zero cuts as the base case through at least Q3 2026.

When is the first realistic window for a cut?

September 15–16 is the earliest date with non-trivial cut probability. That assumes three straight months of disinflation and a June dot plot that signals openness to second-half easing.