Crypto taxes and prediction market taxes get conflated constantly, and the mistake is understandable on Polymarket specifically, since every position is funded, settled, and withdrawn in USDC on a public blockchain. But the underlying tax question is genuinely different from standard crypto taxation, and traders who assume their crypto tax knowledge transfers directly to prediction markets, or the reverse, tend to misreport one or the other. Crypto capital gains tax has a well-established, decade-old framework built on IRS Notice 2014-21. Prediction market gains have no comparable IRS guidance at all, which means the two categories, despite sharing a settlement currency on Polymarket, are being taxed under fundamentally different levels of legal certainty.

This guide covers how crypto is taxed in the US under the established framework, how prediction markets are taxed under a framework the IRS has never directly addressed, and what multi-asset traders holding both need to reconcile on a single return. For the platform-specific mechanics of how Kalshi's regulatory status changes this analysis, Kalshi taxes explained: reporting prediction market profits covers the Section 1256 question in full.

How Crypto Is Taxed in the US: The Established Framework

Crypto taxes rest on a foundation the IRS laid down in 2014 and has built on consistently since: cryptocurrency is property, not currency, for federal tax purposes. That single classification, confirmed in IRS Notice 2014-21, determines almost everything else about how crypto gains and income are calculated and reported.

Capital gains and holding periods

Because crypto is property, selling it, trading it for another crypto asset, or spending it all trigger capital gains treatment, with the tax rate determined by how long you held the asset before disposing of it.

This distinction is the single biggest lever available to crypto holders for reducing their tax bill. On a $100,000 gain, the difference between the top short-term rate and the top long-term rate works out to roughly $17,000, which is why holding period management is one of the most commonly discussed crypto tax strategies.

What counts as a taxable event

The dominion and control standard, most clearly articulated in Revenue Ruling 2023-14, governs exactly when staking and similar rewards become taxable: the moment you can freely transfer, sell, or otherwise use the tokens, not necessarily the moment they're technically earned. Locked or vesting rewards aren't taxed until that lock lifts.

DeFi complications

Decentralized finance activity, liquidity pools, lending protocols, liquid staking derivatives, adds a layer of ambiguity the IRS has not fully resolved. Minting or redeeming a liquid staking token like stETH may or may not constitute a separate taxable disposal depending on the specific mechanism, and this remains an area where practitioners take a conservative reporting approach precisely because official guidance doesn't yet cover every DeFi structure in use.

Reporting mechanics

Crypto capital gains and losses are reported on Form 8949, which rolls up to Schedule D. Income items, staking rewards, mining income, airdrops, are reported on Schedule 1 as other income, or on Schedule C if the activity rises to the level of a business. Starting with the 2025 tax year, centralized exchanges are required to report your transactions directly to the IRS via Form 1099-DA, and a mismatch between what you report and what the exchange reports can trigger an automatic notice. Crucially, crypto losses are not subject to the wash sale rule that applies to stocks, meaning you can sell a losing position and immediately rebuy it while still claiming the loss, a strategy unavailable in traditional securities markets.

For the enforcement mechanics specific to how blockchain activity gets traced back to individual taxpayers, which applies to both standard crypto holdings and Polymarket's on-chain USDC activity, 10 ways the IRS can find your Polymarket tax gains covers this in detail.

How Prediction Markets Are Taxed: The Unsettled Framework

Prediction market taxes operate under a completely different level of certainty. The IRS has issued no guidance specific to event contracts, whether traded on a CFTC-regulated exchange like Kalshi or a crypto-native, offshore platform like Polymarket. This absence of guidance is the central fact that shapes everything else in this category.

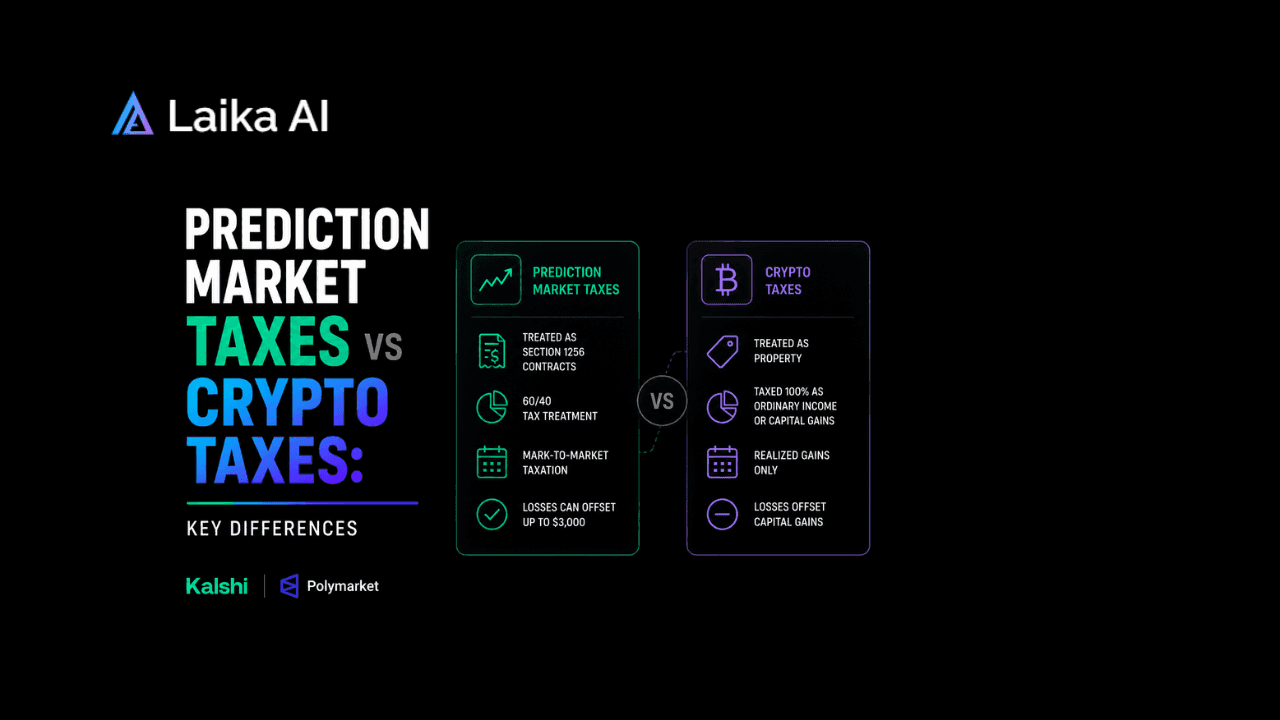

Three competing classification frameworks

Section 1256 treatment is a meaningfully stronger argument for Kalshi specifically than for Polymarket, precisely because Kalshi's CFTC designation is the regulatory hook the argument depends on. Polymarket has no comparable US regulatory status, which makes most tax professionals treat its gains as more likely falling under short-term capital gains or gambling income analysis rather than the 1256 split.

The USDC layer unique to Polymarket

This is where prediction market taxes and crypto taxes genuinely overlap, and where the biggest practical complication sits. Polymarket settles entirely in USDC on Polygon, and USDC, despite being pegged to the dollar, is treated as crypto property under the same Notice 2014-21 framework covering every other digital asset. That means Polymarket activity creates two independent layers of taxable events stacked on top of each other.

The USDC layer is usually near-zero in dollar terms because the peg holds, but "usually negligible" is not "automatically exempt from tracking." When USDC has depegged, most notably during the March 2023 Silicon Valley Bank collapse when it briefly traded around $0.93, that gap between cost basis and disposal value becomes a real, reportable capital gain or loss. Kalshi traders never encounter this second layer at all, since Kalshi settles in US dollars directly. This is the single clearest structural divergence between the two platforms and the primary reason Polymarket tax mistakes and Kalshi tax mistakes look genuinely different in practice, as covered in common tax mistakes Polymarket traders make and common tax mistakes Kalshi traders make respectively.

Documentation gap

Neither platform's documentation practices match the maturity of standard crypto exchange reporting. Polymarket issues no tax forms of any kind to US users, not a 1099-B, not a 1099-DA, not anything. Kalshi's documentation is described inconsistently even among specialized tax preparers, with confirmed issuance of a 1099-INT for interest but genuine disagreement over whether a comprehensive 1099-B covers event contract activity specifically. Compare this to standard crypto exchanges, which are now required to issue Form 1099-DA reporting both proceeds and, starting with 2026 activity, cost basis information directly to the IRS. The documentation gap alone is a meaningful practical difference: a crypto trader on a major exchange has a form to reconcile against; a prediction market trader, particularly on Polymarket, is reconstructing the entire record independently.

Side-by-Side Comparison for Multi-Asset Traders

Practical reporting guidance for holding both

If you trade both standard crypto assets and prediction markets in the same tax year, keep the categories analytically separate even though Polymarket's USDC settlement makes them feel connected. Report standard crypto capital gains and income on Form 8949, Schedule D, and Schedule 1 using the well-established rules above. Report your Kalshi or Polymarket gains under whichever framework you and your preparer determine is appropriately supported, using separate documentation for the prediction market layer itself. For Polymarket specifically, maintain a parallel USDC cost basis record distinct from your prediction market contract record, since the two are technically independent taxable layers even though they usually net to similar dollar amounts.

Are prediction markets taxed like crypto? Only partially, and only on Polymarket's settlement layer. The event contract itself, the actual bet on an outcome, is not taxed under the same established framework that governs standard crypto capital gains, because the IRS has never extended Notice 2014-21's logic to cover binary event contracts specifically. For a full breakdown of how this compares against a third category entirely, traditional sports betting, prediction market taxes vs sports betting taxes covers where gambling-specific rules diverge from both crypto and prediction market treatment. A crypto tax calculator like cointracker.io can help reconcile the standard crypto layer, though it will not resolve the prediction market classification question, since that remains a legal judgment call rather than a calculation.

Frequently Asked Questions

Are prediction market gains taxed like crypto gains?

Not directly. Standard crypto gains follow an established capital gains framework confirmed by IRS Notice 2014-21, with clear short-term and long-term holding period rules. Prediction market gains have no comparable IRS guidance, and the classification, ordinary income, capital gains, gambling income, or Section 1256, remains an open question that tax professionals address by analogy to existing rules rather than direct authority. The overlap only exists on Polymarket, where the USDC settlement currency itself is taxed under the standard crypto property framework as a layer separate from the prediction market gain.

Is USDC on Polymarket treated as crypto for tax purposes?

Yes. Despite being pegged to the dollar, USDC is property under the same IRS framework covering all digital assets, and every acquisition or disposal of USDC in connection with Polymarket activity is technically its own taxable event. In practice the gain or loss on this layer is usually negligible because the peg holds, but it must still be tracked, and it becomes materially non-zero during a depegging event.

How do I report both crypto and prediction market gains on the same return?

Keep the two categories separate in your records even if they interact, as they do on Polymarket. Standard crypto gains and income go on Form 8949, Schedule D, and Schedule 1 following the established capital gains and holding period rules. Prediction market gains go on whichever form corresponds to the classification framework you've determined applies, Form 6781 for Section 1256 treatment or Schedule 1 for ordinary income treatment, with Polymarket traders additionally maintaining a separate USDC cost basis record layered underneath their contract-level activity.

What is the biggest tax difference between prediction markets and crypto?

The level of legal certainty. Crypto taxation rests on over a decade of IRS guidance starting with Notice 2014-21, with clear rules on holding periods, staking, airdrops, and reporting forms. Prediction market taxation has zero IRS-specific guidance, leaving classification as an open legal question that reasonable tax professionals answer differently depending on the platform and the trader's specific fact pattern.

Does the wash sale rule apply to prediction market contracts the way it doesn't apply to crypto?

The wash sale rule currently does not apply to standard crypto assets, allowing traders to sell a losing position and immediately repurchase it while still claiming the loss. Whether this same exemption extends to prediction market contracts depends entirely on which classification framework applies, since the wash sale rule's applicability is tied to whether an asset is treated as a "security" under the relevant code section, a question that has not been specifically addressed for event contracts either.

Where can I discuss prediction market vs crypto tax questions with other traders?

Crypto tax communities and prediction market-focused forums on Reddit both carry active discussion, though the two communities tend to talk past each other somewhat, since crypto traders are usually working from well-established rules while prediction market traders are navigating genuinely unresolved questions. Cross-posting a Polymarket-specific USDC question in a general crypto tax community can produce confidently stated but inapplicable advice, since the underlying legal uncertainty doesn't exist in standard crypto contexts the way it does for event contracts.

The Bottom Line

Crypto taxes and prediction market taxes share a currency on Polymarket, but they do not share a legal foundation. Crypto capital gains rest on over a decade of established IRS guidance with clear holding period rules, defined reporting forms, and increasingly comprehensive third-party reporting through Form 1099-DA. Prediction market gains rest on no IRS-specific guidance at all, leaving classification as a genuine judgment call that varies by platform, with Kalshi's CFTC status supporting a stronger, though still contested, argument for favorable Section 1256 treatment than Polymarket's offshore, crypto-native structure can support.

The practical takeaway for anyone trading both: treat them as separate reporting problems, even on Polymarket where they're mechanically intertwined through the USDC settlement layer. Apply the well-established crypto rules to your standard digital asset holdings, and apply a deliberately chosen, professionally reviewed classification framework to your prediction market activity, since that second category doesn't have an established rulebook to default to.

This article is educational and does not constitute tax, legal, or financial advice. Consult a qualified tax professional before filing based on any framework described here.

Track your crypto and prediction market positions together in one place with Polymetric by Laika AI, so your tax reporting starts from organized, reconciled data across every platform instead of piecing it together at filing time.