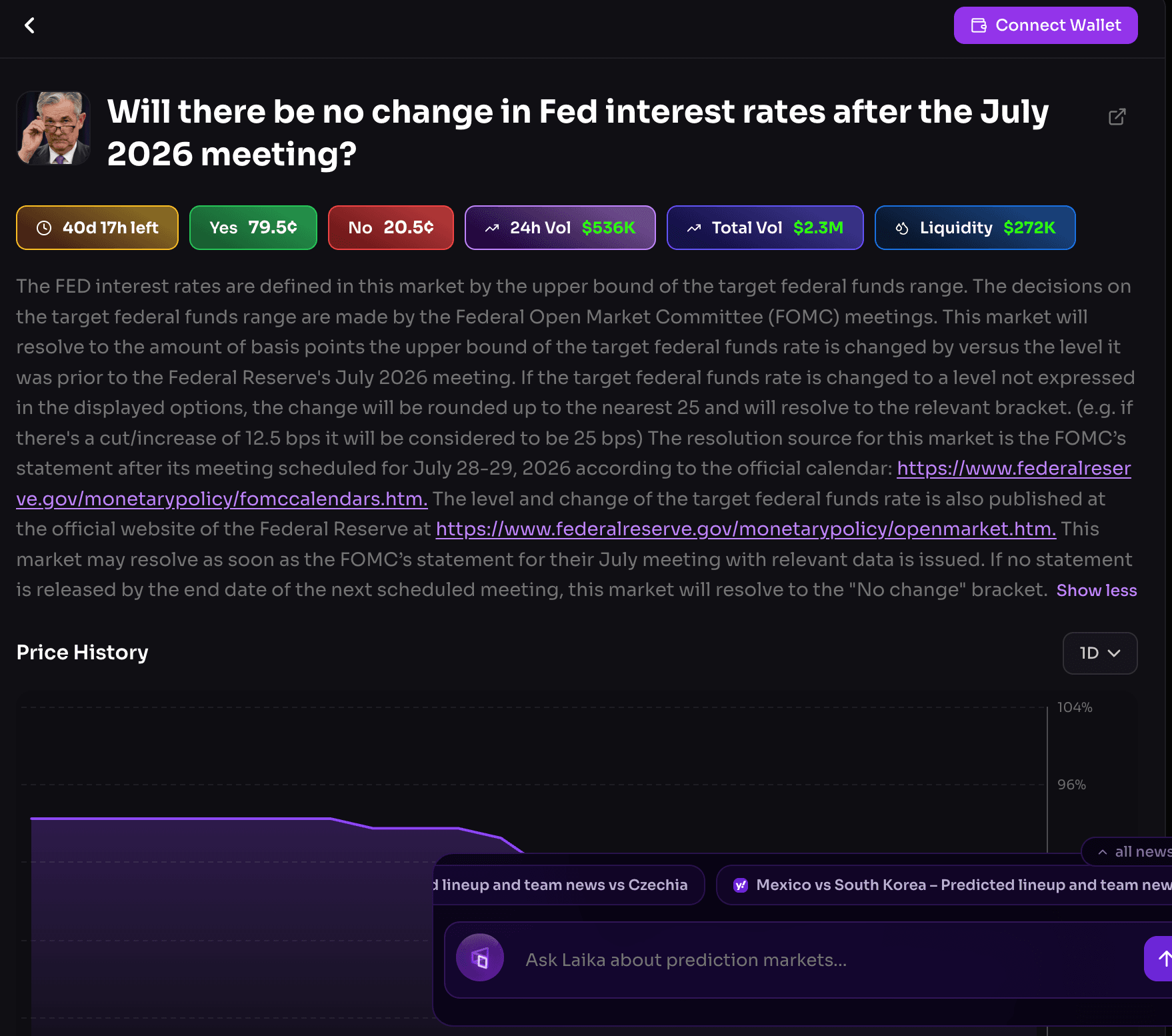

You see a Fed meeting market on Polymarket showing 99% no change. The news is full of macro drama. And it is not obvious what actually matters for prediction market prices: the rate decision, the statement, the press conference, or the future path of policy.

The practical answer is that the headline decision is often already priced in. The tradeable surprise is usually in what the Fed communicates about the future path of rates, inflation, and risk. On FOMC days, the market can barely react to the decision itself and still move sharply when the statement, dot plot, or press conference changes expectations about what comes next.

Start With the Market-Implied Probability, Not the News Narrative

If a Fed meeting market says 99% probability of no change on Polymarket, traders are pricing the hold as overwhelmingly likely. In a binary prediction market, the price is the crowd's implied probability. A contract trading near $0.99 represents roughly a 99% chance of that outcome before fees and small frictions.

Kalshi's Fed decision markets work similarly but often split the meeting into mutually exclusive buckets: maintain rate, cut 25 basis points, or hike 25 basis points. Only one bucket can resolve YES.

A market at 99% no change is not saying nothing will happen. It is saying the specific rate decision is almost fully expected. If you are trying to understand what can still move prices, ask a different question.

What part of the meeting could still surprise the market's view of the future path?

That is almost always where the action is.

Separate the Fed Meeting Into Three Layers

For prediction market purposes, an FOMC day has three distinct layers that do not matter equally.

Layer 1: The rate decision

The simplest part. If the market has 99% on no change, a hold is mostly priced in. If the Fed does exactly that, the contract tied to the meeting's decision will not be a major source of surprise.

Kalshi's standard Fed contracts are tied to the official target federal funds rate as published by the Fed, often using the upper bound of the target range. The contract rules matter here. Above 4.25% means strictly above 4.25%, not equal to it. Always check the exact market page and rules to confirm whether you are trading the rate level after the meeting or the size of the move at the meeting.

Layer 2: The statement and projections

This is where the market often learns whether the Fed is more hawkish or dovish than expected. The statement can change the market's view even if the rate is unchanged. Traders watch for changes in inflation language, changes in labor market language, changes in the risk balance, and changes in forward guidance.

If the statement sounds more concerned about inflation than expected, later rate-cut contracts can fall even though the current meeting was a hold. If the statement sounds more open to easing, later contracts can rise.

When the meeting includes the Summary of Economic Projections and the dot plot, markets focus on whether the median path implies more or fewer cuts than previously priced. This is often more important than the current meeting's decision.

Layer 3: The press conference

The press conference is where the Chair explains how conditional the decision is, whether inflation or employment is the bigger concern, whether the Fed sees one meeting as a one-off or the start of a path, and how it interprets new data or shocks. That means the press conference can move later-meeting contracts, year-end rate-path contracts, and related macro markets even when the current meeting's decision is a foregone conclusion.

If the rate decision is already known, why does the press conference still move prices? Because the market is pricing the path, not just today's number.

What "Already Priced In" Actually Means on FOMC Day

Priced in does not mean the market knows the future with certainty. It means the current price already reflects the most likely outcome and a range of alternatives.

A practical reading: if a hold is at 99%, the market is saying the hold is the base case. If the Fed holds and says nothing surprising, the meeting is mostly a confirmation event. If the Fed holds but sounds more hawkish or dovish than expected, the market can still reprice the next meeting, the rest of the year, or the terminal rate.

The key distinction is this:

Decision surprise: the Fed does something different from the priced-in outcome.

Communication surprise: the Fed says something that changes the expected path, even if the decision itself was expected.

The second type is usually the more important one on modern FOMC days.

A Concrete Example: 99% No Change, But the Press Conference Still Moves Prices

Suppose Polymarket shows 99% no change for the current meeting.

Scenario A: the Fed holds and the statement is neutral. The market barely moves. The outcome was already expected and the language did not change the expected path.

Scenario B: the Fed holds but the statement removes a dovish phrase. Traders may infer the Fed is less willing to cut soon. Even though the decision was unchanged, later-meeting contracts can fall because the market has to reprice the odds of a future cut.

Scenario C: the Fed holds but the Chair says inflation progress is not enough yet. This can matter more than the statement itself. The press conference pushes the market toward a more hawkish interpretation, especially if the Chair emphasizes that future cuts are conditional on more data.

Scenario D: the Fed holds but the Chair sounds more open to easing than expected. Even with no change today, later contracts can rise because traders now believe the next move is more likely to be a cut, or to come sooner.

The lesson: the meeting outcome and the market-moving information are not the same thing.

What Is Tradeable and What Is Just Narrative

This is the most useful filter for anyone trading Fed prediction markets.

Usually tradeable in standard Fed decision markets:

The target rate after the meeting, the size of the move at the meeting, whether the Fed cuts, holds, or hikes, and sometimes the number of cuts by a date or the rate level by a date. These are the events that standard Kalshi or Polymarket Fed contracts are built around and will settle on.

Usually not directly tradeable in the standard decision market:

The tone of the press conference, the exact wording of the Chair's answers, whether the Chair sounds confident or cautious, and the broader macro narrative around inflation, energy, geopolitics, or growth. These are important for price moves but they are not the settlement event unless the market explicitly says so.

That distinction matters because traders often assume the Fed meeting market includes everything said that day. It usually does not. The market may react to the press conference, but the contract may still settle only on the rate decision or a clearly defined rate level. Read what the contract actually resolves on before trading.

How to Read the Market Before the Meeting

Before the announcement, work through this in order.

Check the current meeting contract. Is no change near 99%? Are cut and hike buckets tiny? If yes, the decision is not where the uncertainty lives.

Check the next meeting or year-end contracts. These often matter more than the current meeting. If the current meeting is fully priced, the next meeting may still have meaningful room to move.

Check whether the market is on the decision or the path. If the current meeting is nearly certain, the real tradeable information is usually in later meetings, the dot plot, or the press conference and its effect on subsequent contracts.

Read the exact market rules. On Kalshi, the contract may resolve on the Fed's published target range. On Polymarket, the market description and oracle rules determine what counts. Do not assume Fed meetings mean the same thing across platforms.

How to Read the Market After the Announcement

After the statement and press conference, ask three questions in sequence.

Did the Fed do what was expected? If yes, the current meeting contract may barely move.

Did the Fed change the expected path? If yes, later contracts can move sharply even if the current decision was a hold.

Did the press conference confirm or reverse the first reaction? Sometimes the statement looks dovish but the press conference sounds hawkish. In that case, the first move can be reversed. This is why FOMC days often have a two-step reaction: first move on the statement, second move on the press conference.

Edge Cases Worth Knowing

The meeting is canceled or rescheduled. Kalshi's rules can specify what happens if a scheduled meeting does not occur. Read the exact market text rather than assuming the calendar alone controls settlement.

The rate is unchanged but the target range definition matters. Some contracts use the upper bound of the target range. If you are thinking in terms of the midpoint or effective rate, you can misread the market. Check which rate definition the contract uses.

A press conference market is separate from a rate market. If a platform lists a contract about what Powell will say or signal, that is a different market from the rate decision. Settlement events are different. Do not mix the two.

The Chair changes, but the market is still about the meeting outcome. A new Fed Chair can matter for narrative and expectations, but the contract still resolves on the defined rate outcome unless the market explicitly references something else.

A Practical Checklist for Any Fed Meeting Market

Before entering any position on a Fed decision market, work through these five questions.

Is the current meeting outcome already near 100% priced in? If yes, are later meetings or year-end contracts where the real uncertainty sits? Does the market contract settle on the rate decision, the target range, or a specific statement? Is the likely surprise in the statement, the dot plot, or the press conference? Are you reading the exact platform rules, not just the headline title?

If you can answer all five, you will know whether the market is trading the headline event or the more important sub-event underneath it.

The Main Takeaway

For Fed meeting prediction markets, the headline rate decision is often the least interesting part once the market has already assigned it a 99% probability. The real price moves usually come from what the Fed says about the future path, especially in the statement, projections, and press conference.

The right question is not whether the Fed will cut or hold. It is what is already priced in for this meeting, and what part of the Fed's communication could still change the expected path.

That distinction turns a noisy macro story into a usable prediction market signal.

For a complete breakdown of Polymarket trading strategies across every major market category including macro, sports, politics, and crypto see Polymarket Trading Strategies.

If you're looking for the best crypto-based prediction market platforms and how they compare for macro and event trading, see Best Crypto Prediction Markets.