Prediction Markets Place 96% Odds Against a US-Iran Diplomatic Meeting by June 2026 as Geopolitical Uncertainty Dominates

Last Updated

April 20, 2026

Prediction Markets Place 96% Odds Against a US-Iran Diplomatic Meeting by June 2026 as Geopolitical Uncertainty Dominates

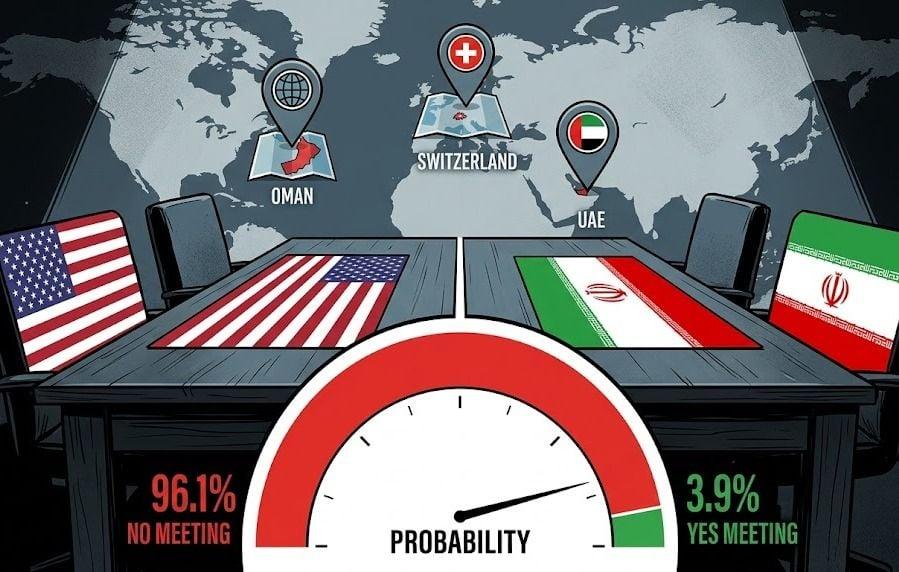

A prediction market tracking the likelihood of a formal in-person diplomatic meeting between the United States and Iran by June 30, 2026, is currently pricing the probability of no qualifying engagement occurring at 96.1%, reflecting deep market skepticism about the pace of diplomatic progress despite the fragile ceasefire that has paused active hostilities between the two nations.

What the Market Is Measuring

The prediction market's resolution criteria are specific and demanding. A qualifying meeting is defined as an in-person diplomatic engagement between authorized representatives of both the United States and Iran that is either publicly acknowledged by the respective governments or reported by credible media sources. The deadline is June 30, 2026, at 11:59 PM Eastern Time. If no such meeting occurs by that threshold, the market resolves in favor of the no-meeting outcome, regardless of how close negotiations may have come to producing one.

That specificity matters because it excludes several categories of diplomatic activity that might superficially appear to be progress. Back-channel communications, third-party mediated exchanges such as the Pakistan-hosted Islamabad talks, written proposal exchanges, and public statements of willingness to negotiate all fall outside the resolution criteria unless they culminate in a confirmed in-person engagement between authorized representatives of both governments. The market is not pricing diplomatic activity broadly, but a very specific class of direct bilateral meetings.

At 96.1% for no meeting and 3.9% for a meeting occurring at some venue, the current distribution reflects the aggregated judgment of participants who have assessed the gap between where US-Iran relations stand today and the threshold required for a direct bilateral diplomatic meeting to materialize within the remaining window.

Comments (0)

No comments yet. Be the first!